CLOs where is your content?

2

10 Jan 2013

NFC is a beautiful technology with uses far beyond payment. In the payment use case however, it is not the technology, but rather a business battle over control and ownership (a 12 Party NFC Supply Chain Mess) which has conspired to create many forces against NFC’s payment success.

As I stated yesterday, latest news is that MCX has chosen QR code based approach from Gemalto (following Starbucks success). My guess is that Gemalto has developed a one time use QR code that is derived from device information (it will change for every transaction… ). You can safely assume that ACH will be the primary funding mechanism (just as in Target’s Redcard and Safeway’s FastForward). The banks had some idea of MCX’s plans are thus moving aggressively to create a directory service to “protect” customer DDA information via tokenization. My guess is that this protection will come at a price….

Here is my best guess of the transaction flow (assuming the rumor is true).

Registration

Usage

I like QR codes for their ubiquity and established consumer behavior (thank Starbucks in the US). Stores don’t need to buy any new hardware for this to work, there is a zero cost of issuance, and it will work on a broad spectrum of phones. Development cycles for Store POS software are normally 18 months… so it could be some time before we see something come out.

QR codes may not be rocket science, but NFC has demonstrated the downside of tech heavy solutions. We may not need a $400M F22 when a simple bicycle will do. Carriers face a future as dumb pipes, a future share by banks, as both work to control their market positions instead of delivering value. MNOs and Banks (in the US) have proven themselves equally incapable of succeeding with new walled garden strategies. Commerce will find the path of least resistance, like a mighty river…

The big challenge for MCX will NOT be in technology, but rather a consumer value proposition. Retailers stated goal is to bring death to merchant funded bank card reward programs. What will convince me to part with my Amex card at the POS?… it will need to be something substantial.

Another often asked question is can MCX keep a bunch of fierce competitors working together in the same tent? This approach seems broad enough to insulate MCX from retail competitive forces and align them in fighting a common enemy. Per Sun Tzu “the enemy of my enemy is my friend”. Retailers are looking to turn the tables on the 2% “payment tax” on their business. There is serious enterprise commitment to making MCX work, banks will do well to treat them with respect.

Who will lose in this approach?

Other Related Blogs

9 January 2013

I’m sitting in NYC waiting on my plane.. thinking about reputation, not only explaining the importance of a “good one” to my 12 and 8 yr old boys, but also thinking about its broader importance in commerce. Where do I have reputations today?

Throughout history reputations were 100% dependent on relationships. These personal networks were the primary conduit of reputation information. Financial services have benefited greatly, over the last century, from improvements made to reputation portability and standardization.

In this modern era, eBay offers many lessons in relevance of reputation, demonstrating what great things can happen when tools exist to manage it. There are also many negative lessons here. For example in 2004, eBay launched into China. Prior to launch eBay’s risk organization wanted to keep the China community separate from the US. Community separation was a logical recommendation given that reputations take time to build, and dependent on community context. In the US buyers and sellers work for years to build trust and “confidence”. Reputations forged by self-dealing, or other fraudulent practices, were ferreted out. Unfortunately Meg didn’t want this community separation… she wanted one big community. Within weeks Meg saw the downside of operating these 2 together, as fraud shot through the roof.. thus separating the communities and opening the doors for other competitors (See this Stanford University Case Study).

Reputation has a very strong societal and community context. I told my sons that a Chef with a great reputation in New York or Paris means something completely different than a great Chef in a community of cannibals (… well it made them laugh). Markets hold people and money accountable, and the ability to measure and convey a commerce reputation is critical for network growth and efficacy. Banks have long held a central intermediary role in commerce as both a “reputation authority” and a manager of the corresponding risk. For example, letters of credit (LOC) are an instrument extended to a supplier receiving an order from an unknown buyer. After all, receiving an order for 100,000 widgets from a known buyer carries a far different weight that one from one that is unknown. Thus an LOC reduces the risk to the supplier by allowing money to be held by a 3rd party bank while the order if fulfilled.

Another excellent reputation example is in serving the poor at the base of the pyramid. In 1976, Muhammad Yunus created the concept which led to Grameen Bank, a success which resulted in the 2006 Nobel Peace prize (see Wikipedia). Muhammad recognized that lending must be tied to a reputation which is critical to maintain: that within the local community. The Grameen model lends money to a community group, whose individual members are mutually responsible for the loan. This is a fantastic model. What further opportunities could exist if participating individuals could expand their reputation outside of the community?

Modern markets have demonstrated that improving the portability of reputation expands the capital attracted to that market. For example financial markets expanded by specialists operating in a securitized model where risks could be aligned to capital. In retail banking, local markets evolved from local banks to national. Each bank could make rational decisions on where to participate and specialize in this market.

In business-business commerce reputation is a critical factor in the success of JIT inventory, virtual supply chains and vendor managed inventory. Few companies would be willing to let an unknown participant into their network. In the online world, eBay and Alibaba have done a tremendous job building communities around reputation. Wouldn’t it be nice if you could take your reputation with you? For example if Prosper or Zopa could get through regulatory hurdles (see here on their issues), lending could be done in an ad hoc community of investors without a banking license. Commerce would be done based upon your community reputation (eBay/Amazon), and risk would be managed through non financial data from retailers, facebook, MNOs, …

Unfortunately few of the holders of your reputation are incented to share it (in a positive sense). Few people know that there are roughly 4 times the number of negative credit bureaus as there are positive. In other words, every bank and supplier are willing to share their negative customer information (ie didn’t pay their bill), very few are willing to share their positive customer information. In most OECD 20 countries, positive bureaus are not the result of commercial initiative, but rather a legal or regulatory one (Wikipedia Equifax).

In the US we have more of an aggregation problem.. how do we manage multiple reputations. In emerging markets the problem is much different: How do you build any kind of reputation? One of the first problems to crack is identity. How do you assign an ID that sticks? We see many government initiatives around National ID, but this takes time. Is there another number or ID that we could use in the interim? It certainly seems that a cell phone number makes the most sense given its global penetration of 5.3B consumers (75%+ of the worlds population). Could emerging market carriers enable an opt in “reputation” consumer service?

I’d love to see a few companies work toward this end.

In the US, I’d love to see a consumer service that just measures my reputation in all of these places (beyond banking).

Sorry for not finishing this blog cleanly…

Rumor is MCX is going with a “Starbucks model” QR code payment mechanism. Gemalto is rumored to have won the wallet (… arghh why another one?).

There are many Merchant benefits to this approach, primarily it skips the entire bank owned payment network as QR codes are read directly by the ECR (IBM, Micros, Aloha, NCR, ..) with minimal hardware changes. MCX members with Loyalty cards (ex CVS) would be able to skip the phone based wallet and leverage common MCX infrastructure (cloud) to enable payment on loyalty cards.

Fraud infrastructure will be critical to the success of this approach. Retailers have tremendous historical data for loyalty card customers… but they really don’t know who their customers are. Banks are certainly able to help solve this fraud, identity and reputation problem. MNOs may also be able to add value here IF they move quickly (example Payfone would be perfect here).

Another story I heard was the Starbucks was a founding member of MCX, but then left. If this QR code approach is accurate, their departure makes sense.. as they are the team that paved the way for the success of this approach. Why would they throw their technology and standards away for something exactly the same?

The payment mechanics of all this certainly look good. However what will be the consumer value proposition? I hope this QR code can be ported to other wallets (let the customer decide).

2 January 2013 (updated typos and added content on kyc, cloud, and push payments)

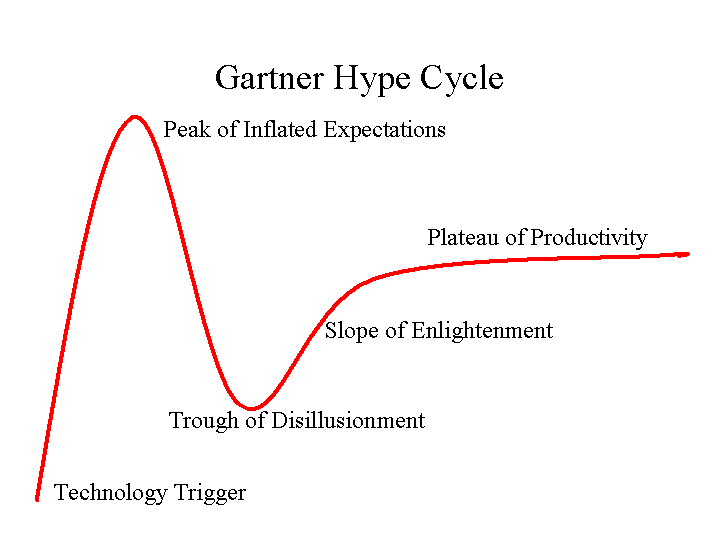

Looking back to my first “prediction” installment 2 years ago, 2011: Rough Start for Mobile Payments, not much has changed. Although I am personally approaching the “trough of disillusionment”. Lessons below are not exclusively payment (ie mobile, commerce, advertising) but seem relevant .. so I mashed them together. Key lessons learned for the industry this year:

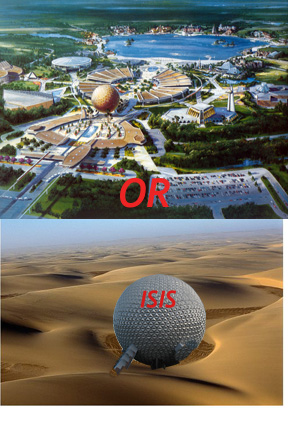

without a compelling value proposition…) and we have our current state (see my Disney in a desert pic). Take a look at who is executing today and you will see product focus around a defined value proposition. My leaders: Square, Amex, Amazon, Sofort, Samsung, Apple, SKT, Docomo and Google. Organizations can’t continue to stick with leaders that are focused solely on strategy, or technology, or corporate development… You should be able to lock any 3 people in a room for a week and see a prototype product. The lack of depth in most organizations is just astounding. Executives need to bring focus.

without a compelling value proposition…) and we have our current state (see my Disney in a desert pic). Take a look at who is executing today and you will see product focus around a defined value proposition. My leaders: Square, Amex, Amazon, Sofort, Samsung, Apple, SKT, Docomo and Google. Organizations can’t continue to stick with leaders that are focused solely on strategy, or technology, or corporate development… You should be able to lock any 3 people in a room for a week and see a prototype product. The lack of depth in most organizations is just astounding. Executives need to bring focus.Predictions

Here are mine, would greatly appreciate any comments or additions.

Happy New Year! Football is on my plate today so this blog will be short.

American Express is cranking out innovation at a tremendous pace. I’m very impressed at what Ken and Dan have done here in last 3 years. For example I just received a note in the mail yesterday that all of my Amex transaction receipts will be in my Apple passbook (don’t know why they used the USPS to tell me). Here are a few other innovations

Retailers don’t like the costs of Amex… but they love Amex customers. Amex has a very heavy bias toward business and T&E spend. Although Amex has only 12% of global card payment volume, each Amex customer spends more than 4x the amount of a typical V/MA holder. In full disclosure I own Amex stock, and I’m an Amex points junkie.![]()

![]()

Amex is working to expand its consumer base (into mass) through Bluebird and Serve, but I won’t go into that here.. What I’m most impressed with is that they are the first card network that is beginning to deliver value to advertisers and retailers…. Yes, through its massive trove of consumer insight, Amex is beginning to show signs that it can deliver value to retailers.

Following on from my Nov Blog: Retail CRM Enabled by Payments, Amex’s recent loyalty partners acquisition is showing signs of success in coupling merchant transaction data with its DataInsights business. Through this, merchants have new mechanisms to identify customers, incent loyalty and market specific products.

In my view, Amex is at least 5 years ahead of any other issuer/network. Of course they have the benefit of operating as a 3 party network and regulated bank. This allows them to own: the consumer, the merchant and the rules of the network. As such they have many “innovation” advantages over the V/MA networks and issuers; Amex’s network is much more pliable, where the 4 party networks are very hard to change.

This same dynamic is why Discover is the “dance partner” of choice for anyone working to do something unique at the POS. It is also why I see a 3 party network as the winner of MCX (?a NEW 3 party network?). As I stated previously, innovations at the POS will be less about payments and more about data and re-orchestrating commerce to create new experiences. There are 3-4 entities that each have unique data, none of which have shown interest in pulling it together: retailers, bank, advertiser, telecom.

Amex is the first to start breaking down this data “log jam” with willing participation from retailers. Although their consumer segment is very narrow, margins are tremendous in this top tier.. which means Amex could be in a position to further accelerate its affluent value proposition without mainline retailer participation (ex focus on T&E).

Random thoughts for Investors

Sorry for typos and short blog