© Starpoint LLP, 2022. No part of this site, blog.starpointllp.com, may be reproduced or retransmitted in whole or in part in any manner without the permission of the copyright owner.

Given that 80% of my payments thoughts over the last month have been on identity it is time to move on to settlement. Understanding the process of settlement is key to understanding both payments and banking.

Today’s blog hopes to address 4 questions

- What are the fundamental innovations in settlement?

- How will innovations change competitive dynamics?

- How will innovations change political dynamics?

- What flows will be impacted?

Nobel economists Coase/Williamson demonstrated how transaction costs shaped the Nature of the Firm. Settlement systems define the transaction costs of finance. Thus settlement system design shapes the organization of financial services. Settlement is in the midst of a revolution as many parties seek to remake settlement as the “base” platform capable of unbundling financial services.

Settlement provides the legal structures and operating rules required to clear $USD Trillions per day are 95% across multiple parties. Banking is a connected business, if the world was in a single account there would be no settlement issues as everyone would be on the same ledger.

As with all networks increasing scale results in increased network rigidity and existing participants consider how changes impact the value they receive and their unique competitive dynamics. For example, many of the proposed changes to settlement will impact correspondent banking. While some see opportunities to reduce the “cost” of correspondent banking, others providing the correspondent services see change as a reduction in revenue. While the tech of settlement is fascinating, at the end of the day one counterparty has to trust the netting process to permit funds to flow from their account.

While there is no near-term cliff, settlement innovations may result in a dramatic shift of payment volume. Today V, MA, SWIFT, EFT, … ALL run on the same settlement process. As most of you know, there is over $4T of market cap driven by networks residing on TOP OF settlement. For example, card networks do not move funds, but rather are messaging networks. While the legal and operational structure of settlement may not change, a change in technology can have significant implications for how messages operate between trusted parties and the DIRECT ACCESS of non-banks (ex PSPs, non-banks, …etc.).

This is a HIGHLY POLITICAL undertaking, with many change advocates working to reduce the power of US/EU banks and sanctions controls. Changes in settlement have the potential to unbundle banking, payments drive changes to central bank power and FCY reserves. Where open banking breaks open the FRONT END, settlement remakes the back end. For example, if risk in settlement can be managed by specialists commercial/retail banking (and payments) could move toward a model which resembles modern financial markets (clearing process is a commodity).

Key Points

-

- Settlement is the core of finance and a bank’s role in brokering “trust” between counterparties.

- As the “core” there are many parties seeking to remake settlement as the “base” platform capable of unbundling financial services. In my view, David Marcus’ Libra is the reference operating model which others are iterating from (see blog). The Bank of International Settlements (BIS) innovation project list provides a small window into the future.

- Environmentally there are multiple forces at play in this redesign.

- Immutable Money – Stablecoins/CBDCs

- Technical – DLT/Web 3.0. Decentralization is a central tenant of Web3. Within finance, this web 3.0 decentralization is manifested within DeFi and DAOs (see blog).

- Networks – Decreasing cost to connect, ability to manage more connections, and Increased number of specialist networks AND bi-lateral agreements

- Political – particularly organized central bank efforts to insulate against sanctions. The key example is eCNY and China’s Cross-Border Interbank System (CIS Paper)

- Unbanked – Central Bank success stories UPI/PIX (blog)

- Speed – Central Bank RTGS/FedNow, TCH RTP, UPI

- Auditing and Verifiability (DLT)

- Regulatory – OpenBanking/Open Payments, Central Banks role expansion

- Mobile Platform/Identity (blog)

- Costs of Financial Intermediation are at an all-time high. (see blog and work of NYU’s Thomas Phillippon)

- As with all things tech, the best way to discern progress is an assessment of HOW the big players are constructing competitive advantage (ie operational, financial, …etc)

- Standardized banking and payment products (ex cards) establish trust through an operating model which allows the bank to intermediate, reduce risk and create a legal regime for value exchange and stakeholder investment. A one size fits all trust structure is rapidly becoming unbundled as identity, trust (ie legal agreements) and risk are managed outside of banking (ie bank disintermediation).

- Connecting to a network requires ENERGY and each entity is thus cost constrained in the number of networks and external affiliations. Technology has decreased transaction costs and expanded the ability of nodes to connect to multiple networks (ie mobile). As outlined in Small Wins, Nobel economists Coase/Williamson demonstrated how transaction costs shaped the Nature of the Firm. Settlement systems define the transaction costs of finance.

- Thus settlement system design shapes the organization of financial services. (see Transformation of Commercial Networks: Unlocking $2T).

- BIS innovation demonstrates new models for bank settlement, many of these innovations can be extended to non-banks which could lead to a potential revolution in how settlement can be performed between all trusted parties (ie, non-banks, see Libra blog). For example, most large multinationals have global supply chains with deep contractual relationships and significant finance/treasury services operating across global financial networks. Amazon, GE, Google, and Daimler all manage inbound/outbound flows and cash across domiciles. What transactions do they settle centrally? What do they settle locally? While the technology is impressive, there is little likelihood of 10%+ volume transitioning to any new bank settlement model in the next 20 yrs.

- The political context for settlement innovation requires critical inspection. Emerging market central banks seek greater role in cross border for greater control and insulation from US/EU currencies/controls (ex sanctions). The ability for a central bank to monitor every transaction is powerful.. And potentially Orwellian.

- As I outlined in Innovation in Networks, expect to see new technology gain traction first by existing players to create a competitive advantage. These problem spaces are at the leading edge (ex JPM’s ONYX). Thus the core flows at risk near term are not inter-bank but non-bank flows that will be driven by focused hubs and central banks (ex Amazon, Alipay and ASEAN Central banks).

- Historically only a single centralized entity could ensure risk-free settlement. Today’s settlement processes are net settlement, protecting the privacy of transaction detail and counterparties. A primary disadvantage of most shared ledgers (ie DLT) and CBDCs (most do not operate on blockchain) is the centralization of information (see ECB white paper and World Bank)

- In the next 20 yrs, we will see a shift to decentralized settlement in trusted flows. Near term, investors should expect commerce concentrators (Supply Chain, Apple, Amazon, …etc) to expand their role in settlement by leveraging many of the same technologies envisioned by BIS. (example start up – Softbank funded TBCASoft)

- A metaphor for Decentralized Settlement is bi-lateral contracts. For example, supply chain agreements manage the risk of value exchange between known and trusted parties. Large enterprises have complex global cash management operations with local bank accounts and local FCY reserves. A supply chain network is a settlement network, and banks’ role will greatly decrease here as new settlement approaches enable enterprise treasury management.

- Globally, Central Banks will take a much more involved role as few banks have proven the ability to serve the bottom of the pyramid (ex India’s UPI), and cash displacement enables greater monetary controls and taxation. While existing payment networks will benefit (ex V/MA 44% growth in India), opening of settlement networks to non-banks also creates competitive threats to high margin bank lines as specialists take on the risk, just as they do in competitive financial markets.

- What flows are most likely to be impacted in the next 5 yrs?

- High trust flows: Supply chain, recurring payments, marketplaces, large merchants (ex Target/RedCard),

- Mobile Payment Platforms/Identity Driven (UPI, PIX, Apple, Google, Alipay, …etc),

- Underbanked/Remittances

- Trade Flows with China (ex eCNY in Oil Contracts see CIS Paper)

- Government flows

Background – Settlement 101

From a financial perspective, Settlement is the process of completing a transaction to satisfy the legal conditions under which the exchange value was agreed. Settlement can be bi-lateral, or it can involve neutral 3rd parties that specialize in managing the agreement, transaction, credit, risk, compliance, and …. Etc.

All transactions would settle bi-laterally if there was no risk, no uncertainty and a perfect ability to define and verify value exchanged. But this is never the case. Within the hi-tech and aerospace supply chains contracts are complex, vendors are integrated and with prescribed definition, inspection and certification of purchases. In collectibles and rare art, specialists assessing the authenticity and chain of custody are the focus. The value of a bank is in intermediating risk between parties.

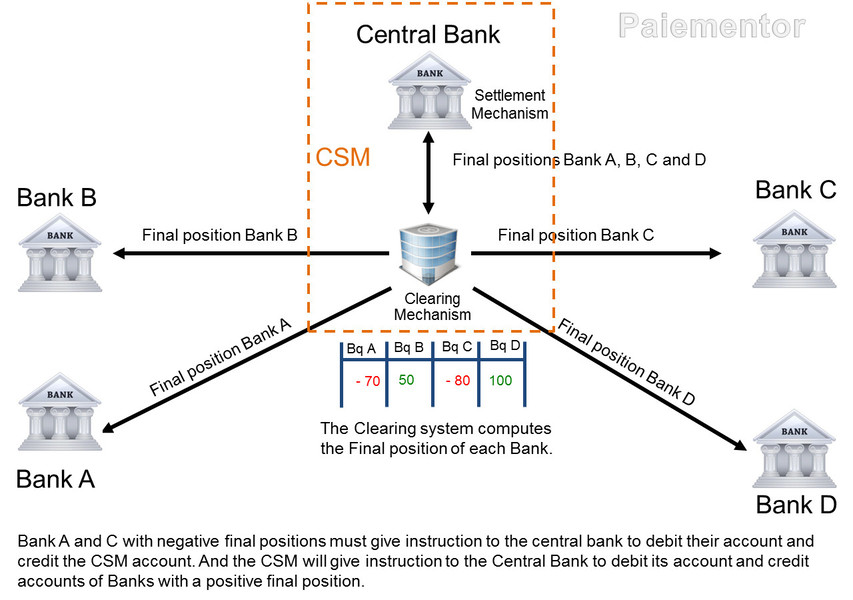

Today’s largest settlement entities are also the largest “trust” networks: The Clearing House (TCH), BACs, NACHA, …etc. Within these associations, members are typically restricted to regulated banks and commit capital in excess of their settlement needs. They must also operate consistently across members within a process approaching “risk-free”. See World Bank Whitepaper on Settlement Models.

To reduce risk and bind settlement “capital” to legally enforceable operating rules the settlement process is typically held within a single organization. In the US, TCH dominates at almost $2 TRILLION per day. This transaction total expands beyond payments, cards, retail/commercial banking activity. For example, TCH Banks also settle funding for Wall Street, and government spending/benefits. It is little wonder that the CEOs of the top US banks take an active role in TCH’s board.

Just as in Commerce, Banks can’t operate in isolation. As accounts are distributed, there must be networks for collaboration. Settlement is a world of multiple ledgers, central banks, hubs and associations. For example, in the US Fed Chartered banks clear bi-laterally, through peer associations (Pariter – WFC/JPM/BAC), TCH, …etc. State chartered banks and state-licensed MSBs clear through state associations, NACHA, …etc. At the end of the day net settlement is done through the Federal Reserve’s National Settlement Service (NSS) which holds the “master” ledger for bank deposits (4.5% min + SCB buffer for Tier 1 Fed Charter).

Settlement solves the n-square problem of direct bilateral connections and creates a consistent legal/operational environment for trust.

Internationally, OECD 20 countries work much the same way. However, in emerging markets, the central bank takes a much more active role in settlement as scale does not allow competition for private associations and the inability to settle can serve as a barrier to entry for new banks. Additionally, emerging market central banks seek finer-grained controls to reduce currency volatility, manage M1/M2 and trade/investment flows.

Cross Border/Multi-Currency (MCY)

It is important to note that not all cross-border transfers go through BIS. In fact commercially, correspondent banking provides the primary mechanism for international settlement. For example, many international banks keep a correspondent account with Citi or JPM for both Visa card settlements and for commercial/financial market transactions. Citibank’s Global Transaction Services (GTS) is the leading player here (CEO calls it her crown jewel – created by FISV’s Frank Bisgnano. See my short video covering cross-border settlement for more info.

BIS Project mBridge Report provides and excellent overview of the state of cross border

[…. bulk of settlement in correspondent banking occurs in commercial bank credit, representing a liability of the commercial bank. As such, it carries the associated credit and liquidity risks where settlement funds may not be available in the event of illiquidity or insolvency. Although the foregoing risk rarely materializes, it becomes significant when aggregated over large values and long settlement periods. Settlement in central bank money, the safest settlement asset, eliminates this risk; however, it is typically restricted to interbank domestic payments on access-controlled central bank real-time gross settlement (RTGS) systems. One exception is Continuous Linked Settlement (CLS), a specialist institution that settles FX transactions on a PvP basis and maintains an account at each of the central banks whose currencies it settles; however, to date only a limited number of currencies are supported. The costs associated with the correspondent banking model are substantial – private sector estimates suggest that, in 2020, for nearly $23.5 trillion in cross-border transaction flows, transaction charges amounted to around 0.5%, or approximately $120 billion (excluding FX costs). Furthermore, adverse secondary effects not captured in this figure, such as settlement delays and risks, likely amount to far greater costs.

As a banker, I shake my head a tad here. As the role of banks is to intermediate flows and assume risk. While the central bank sees cost and inefficiency, large correspondent banks see revenue. Banking products and services are coupled. If BIS/central banks take on a larger role in correspondent banking, commercial banks will change their behavior in currency trading and correspondent lending. Today large recurring commercial flows do not occur on BIS, they run on specialist networks like Citi GTS or in bilateral agreements between large banks.

From a US/EU viewpoint (the politics)

It is NOT the large recurring “high trust” flows that will be impacted by BIS innovations but rather the flows seeking to end run US/EU control (ie sanctions, country bi-lateral, …etc) and low trust flows. Central banks in Asia are supportive of BIS innovation efforts as they provide a path for greater central bank intervention in FCY and a path to manage their own FCY reserves and trade flows. Potentially “redomesticating” enterprise balance sheet capital within their home market.

Central banks participating in BIS innovation efforts have a high degree of influence over their domestic champions. In most cases they seek to increase their role in new cross border settlement systems which reduce dependency on US/EU banks/financial markets. A non-political solution exists for the cross border “problems” today in CLS. But the CLS model does not increase the role of the central bank.. It only makes the existing process more efficient.

From an Asian perspective

“…traditional model of cross-border payments presents even more challenges for emerging market and developing economies (EMDEs). Banks started paring back their correspondent networks and services after the Great Financial Crisis, with smaller economies likely experiencing a greater decline, leaving many without sufficient or affordable access to the global financial system. Furthermore, cross-border transactions are often settled in a handful of dominant currencies and FX trading involving non-dominant currency pairs remains limited.18 This exposes EMDEs to spillover effects from the monetary policies of jurisdictions from which the

foreign currency originates, as well as associated financial stability risks, such as credit cycles. The limited international role of many local EMDE currencies also raises the issue of access to liquidity for these economies in times of global financial turbulence”

Settlement Innovations

There are three excellent white papers on Settlement Innovations

- BIS – Overview and Framework for Use of DLT in Settlement – 2017

- US Federal Reserve – DLT in Payments, Clearing and Settlement – 2016 and

- US Treasury – Future of Money and Payments – 2022

From my perspective there are 6 core settlement innovations

- CBDCs – Immutable Money – Issuance and Redemption

- Legal/Operational – Cross Jurisdiction Synchronization of Action on CBDCs

- Settlement Hub – Distributed Ledger as Tech “Core” for MCY CBDC Settlement

- APIs/Off Ramps – Linking Domestic Banking Systems to Hub

- Transaction Netting and PvP in CBDCs

- Control and Monitoring (the biggest drawback)

I’ll be going through each of these in Part 2.