Money2020 is in 3 weeks. This is the first year that Anil and Jonathan are no longer running the show since selling the conference (see Recode). While I’m anxious to see all of my friends, I’m also anxious to see what the new format will bring. The best year of the conference (IMHO) was 2014 back when it was at the Aria.. the Venetian just made everything too big. Of course I also had the most fun in 14 because I promised Anil and Jonathan that Apple Pay was launching so held a slot for them (6 months prior). This is perhaps my only accurate guess on anything Apple has ever actually done.

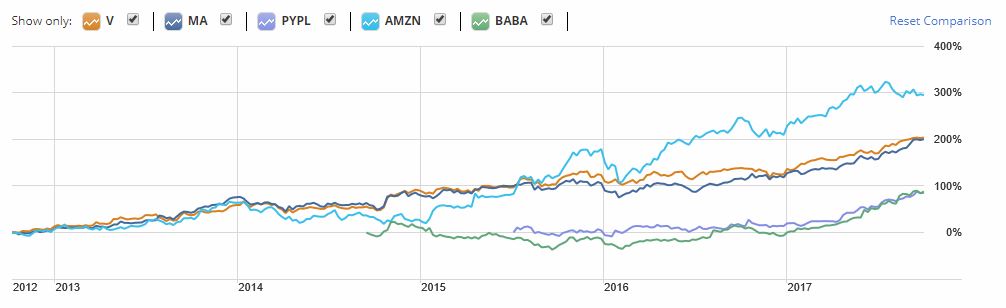

As my investor friends make a list of what to do… so I thought I would make a list “hot things” to look for. Payments and eCommerce have been great investments in last 6 years.

Most institutional investors are looking for threats that would impact their views of risk (beta) and return (alpha). VCs are looking for the next new thing. Start ups are … well looking for attention. As I’ve often stated, payments are a networked business and work very well. They are the key event in commerce where manufacturer, retailer, advertiser, bank, consumer, …etc all claim “SUCCESS”. As I outlined in the Changing Economics of Payments, the beauty in the V/MA 4 party models is shared economics for participants. It is the only scheme where 1000s of business invest billions of dollars to make it work. There are many more logical ways to perform a payment, but none that incent the shared investment in infrastructure and rules.

- Margins in payments are going down, but the impacts of compression are largely hidden by growth rates in the mid to high 20s. Payments are becoming a utility that is “part of the OS”, as payments tokenize identity becomes a proxy for what was a bank issued card. Identity is something that Google and Apple care about deeply, as it is core to commerce value orchestration. Remember consumers want “stuff”.. they go to Amazon and Alibaba because the want to.. they deal with banks because they have to. Banks are becoming dumb pipes and thus lose their pricing power, a power that accelerates when they don’t own identity or issuance (enabling smaller players and more competition).

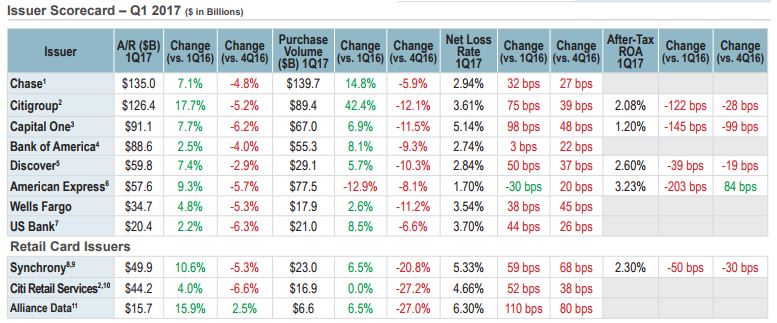

[source: First Annapolis]

[source: First Annapolis] - Data and Artificial Intelligence is focus of Sunday. Banks certainly know how to use AI to help themselves, can they harness it in a way to help others. Another key here is that banks must stop the massive leaks of data. Beyond Equifax, Argus has a copy of every single bank card transaction. Hard to build an AI business when your data is playing (without bank permission). Every attempt to anonymize bank data is met with efforts to de-anonymized. From Verisk Investor Day March 06, 2014

- Collaboration focus for Monday. I told a top 5 global bank last month that Alipay is winning in asia NOT because it is the best payment scheme. Rather it is part of the best commerce value proposition. Amazon, Apple and Google want consumers to pay the way they want to pay.. they are agnostic. Partnership and collaboration is a new core skill for banks, and they don’t do it well today. I will be going to the Mastercard Vocalink and Google Fido, Paypal/Synchrony and the Data Driven Payments presentations

- Identity. My #1 must go to session is Wednesday 8:30am Identity is Fundamental (with Dave Birch)

- Opportunities/Threats. I’m very interested in assessing my assumptions and identifying new threats. Blockchain has the potential to disrupt everything. Is it taking off? I will go to Bill Ready’s presentation on Wednesday How Mobile will Enable Commerce in New Ways, Jim McCarthy’s session on Finding Opps in Today’s Environment, and Monday’s session with Walmart, Google, Cap One and Google Why mobile payments is not gaining steam.

Parting thoughts

Commerce Signals is presenting in 2 sessions, hope to see you there..

- Sunday 1pm Privacy and Data Security – Russ Schrader

- Monday 4:30pm Shakers and Stirrers – Tom Noyes

CORRECTION

In a post entitled “What to expect from Money in 2020” posted on October 5, 2017, I stated that Bank of America had “pulled out of their relationship with Cardlytics”. Cardlytics has informed me that this is false and that there is no change in the relationships with Bank of America or Citi. I

apologize and regret this error.