Bill Pay in the US

Given that Bill Pay is a RTP/FedNow opportunity I thought I’d provide an update into the chaos that is US Bill Pay.

Bill Pay consumer surveys and “market opportunities” are hard to decipher. My summary of the current state:

- Bill payment methods vary by trust, demographic, income level, recurring/one-time and amount.

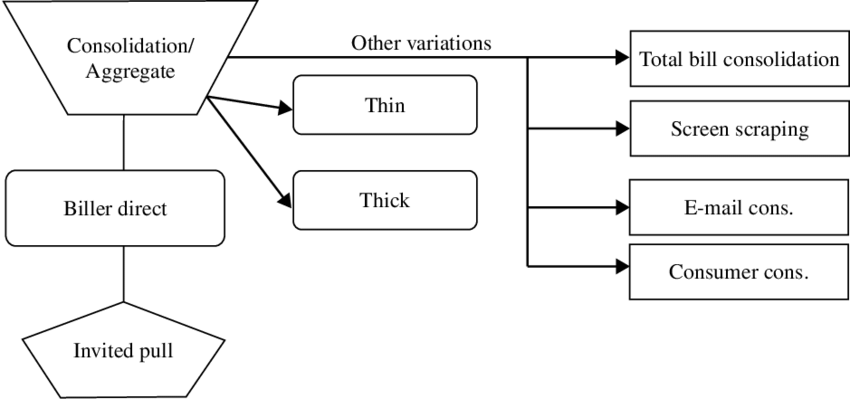

- There are at least 12 different bill payment models (figure below – reference)

- KC Fed Study shows lower income demographics incur high cost of bill pay

- Atlanta Fed Study shows rent payment methods. The amounts here skew other surveys significantly, thus rent/mortgage is frequently excluded.

- Significant differences in bill pay preferences between age cohorts

- Banks’ role in bill payment is decreasing with a very rapid rise of biller direct payment, particularly for one time.

- FedNow could dramatically lower the cost of bill payment.

- Banks want to regain control of consumer bill pay – American Banker

- Remittance information is key for presentment of bill to consumers and reconciliation of payment (see Fed Study)

Twelve Bill Pay Models

- ACH Auto Draft (Invited Pull)

- Check

- Bank as Consolidator/Aggregator (Consolidation – ACH Push with remittance information)

- Payment (no presentment) – Consumer enters in all account information and total to be paid based upon bil their reived outside of the system

- Good Funds – Credit (ex WFC, JPMC) – Payment first leaves consumer’s account, enters a bank suspense/settlement account, then bill paid to biller (3-5 days after initiation)

- Risk Based – Credit (Bank of America) – Bank initiates payment to merchant immediately (1-2 days) – FISV’s Checkfree

- Tokenized RfP – “Debit” (Ex JPMC and Mastercard) – JPMC provisions an RfP or DDA Token at Biller and Biller initiates a request for payment (RfP) or ACH Debit. Instant funds availability IF MERCHANT integrates to JPMC’s wholesale functions. The RfP message would likely also contain remittance information (ie link to bill detail). FedNow could also act in this model but requires merchant bank to integrate. Note in the JPMC model, MA’s finicity would use the link to populate a notice of all bill detail to consumers.

- Card Based Bill Pay – “Debit”. Bank efforts to have bill’s paid by card/virtual card. Focused primarily on supply chain and B2B payments.Ex https://www.billtrust.com/

- Thin – Bank receives bill total amount from biller with link to detailed information. Consumer initiates payment based upon bill received.

- Thick – Similar to above, but the consolidator holds all billing/remittance data

- Provided by biller

- Provided by screen scraping (ex Yodlee Biller Direct, MA’s Finicity)

- Provided by link from biller in RfP transaction (a.iii above)

- Payment (no presentment) – Consumer enters in all account information and total to be paid based upon bil their reived outside of the system

- Biller Direct – Consumer pays bill on billers website

- eMail Bill Pay – Biller sends consumer mail with an embedded payment link (ex ApplePay)

- Non-Bank Consumer concentrator – (Pay anyone) Google in India/UPI, Intuit, SMB focus – RAMP, Mello, Bill.com

Bank Drivers

Bill Pay has always been a money-losing service for banks. During my time at Wachovia, Checkfree was the 3rd largest vendor to the bank (by cost). Consumer banks take on this cost as Bill Pay has proven to be a top three retention method (ie it is sticky and hard to change). It also drives a tremendous frequency of interaction. Within the retail bank, consumers log in about ~5-7 times per week and spend 45 sec – 2 min checking their balance, paying their bills, and leaving. While this virtual “foot traffic” is critical for retailers to sell other goods, it is hoped that consumers will also consider other “offers” (ie Cross-sell) from the bank.

Note that the credit card side of consumer works much differently, with the average consumer logging in only 1-2 times per month.

Naturally, Banks would like to turn this cost into a revenue driver. Within the methods above, debit schemes offer the only alternatives: Card and RfP.

The MDR model for cards is well understood. In the case of RfP, merchants would pay for instant funds availability and reduction/elimination of consumer collections/reversals. With both the FedNow and TCH RTP networks, each bank may set its own fee.

I covered the TCH RfP scenario in JPMC/Mastercard TCH Bill Pay (Nov 2022). The design of the service would provide a fantastic consumer experience with real-time notification of bills, bill detail, and the ability to pay instantly (at the consumer’s discretion). The challenges are in the merchant costs and exceptions. JPMC has roughly 10% of the US consumer retail banking market, It is tough for any merchant to invest in solving a problem for 10% of their consumer base.

Given that FedNow provides the same payment capabilities (without the finicity aggregation/presentment). It would be most logical for a wholesale bank to make the case they could operate across networks (ie any TCH or FedNow bank). I do believe this is JPMC’s Wholesale’s merchant pitch.

Opportunity Lost – Zelle RfP

There is only one operational RfP Real Time service in the US. Zelle RfP. Consumer’s see this today in “request payment”. Logically the Early Warning Product team has proposed the expansion of this success into bill pay. A few of the banks are on board, but unfortunately, this approach conflicts with TCH RTP efforts to onboard merchants to TCH RTP (not Zelle RfP). 1-2 EWS banks thus forced Zelle to stay within a “consumer-only box”.

From my perspective, an obvious solution is to let TCH onboard the merchant for TCH RfP and Zelle onboard the consumer while making Zelle RfP and TCH RTP interoperate (which they do today). I predict this will happen, but the JPMC/MA efforts show that banks would like to see if they can drive solo as they seek to differentiate themselves.

Post Script

Have you ever heard and old song on the radio that brings you back to memories of college or your high school days? The mention of Bill Pay does that for me.. But mostly with negative connotations. Back in 1998, Oracle was building its first 2 Java-based software products iStore and iBill&Pay. My team had iB&P, we were building the product in Redwood, selling and implementing it in Sweden-Telia, Australia-Cardlink, JPMC-Tampa, Israel… Just when I thought left it behind, I became the owner of the second-largest online consumer bill pay bank at Wachovia.

Recommended Reading

- https://javelinstrategy.com/research/us-bill-pay-market-can-financial-institutions-win-back-payers

- https://www.pymnts.com/consumer-payments-2/2023/property-management-firms-reliance-checks-means-more-late-rent-payments/

- https://www.pewtrusts.org/en/research-and-analysis/issue-briefs/2016/05/who-uses-mobile-payments

- https://www.atlantafed.org/banking-and-payments/consumer-payments/research-data-reports/2016/how-do-people-pay-rent

- https://www.kansascityfed.org/research/payments-system-research-briefings/when-paying-bills-low-income-consumers-incur-higher-costs

Slightly unrelated but what do you think the future of B2B bill payments looks like and why?