Short Blog – Free Content

© Starpoint LLP, 2023. No part of this site, blog.starpointllp.com, may be reproduced or retransmitted in whole or in part in any manner without the permission of the copyright owner.

My good friend Dave Birch wrote a piece in Forbes last week on Account to Account transfer threat to V/MA. I wanted to provide an alternate view. This will likely be a multi-part blog.. today I’m starting with the consumer and the merchant (from a US perspective).

No new information for my frequent readers, just pulling together some of the latest data (see PIX below).

Within the US/EU I look at potential threats to Visa/Mastercard this way.

- What problem will the payment “innovation” solve and for whom? Get anyone advocating A2A to answer this question. A merchant-only value proposition (ie cost reduction) does not serve the consumer (see A2A where does it work and why)?

- Speed and Finality are not consumer value propositions!! There is no consumer value proposition in real-time payments. As part of the Fed’s effort to assess market needs (see blog), the only consumer use case they could identify 10 yrs ago was “emergency bill payment”.

- The economic model in payment is the key to success. This is the V/MA innovation. Parties that own risk must be compensated for it. Successful payment networks revolve around a shared and enforceable definition of roles, standards, counterparties, trust and risk. These attributes and the operating model drive scale and participant investment. Regulatory-driven initiatives like SEPA, and PSD2 (open banking) have failed because of this dynamic.

- Customer experience. Today your card information is stored in mobile wallets, in your browser, and integrated into your PC’s operating system. Consumers know how this works. Why on earth would they change? Affirm and credit access does provide a great example of why a consumer would change. A2A? Not even close.

- Collective investment combined with ubiquity. Payments are the easiest part of commerce and are becoming embedded infrastructure (like water/electricity). They are the ONLY ubiquitous payment method in US/EU. As such, V/MA are at the heart of 85%+ of all FinTech innovation because there are economics and rules. Companies like Stripe, Shopify and Adyen have made payments easy. 75%-85% of their revenue is from software services, and payments are becoming a loss leader in a larger bundle. The model for success in the US is Target RedCard (see blog).

- Hurdles – To overcome shared investment and engrained behavior, a 20% improvement in consumer value is required. A survey of successful efforts reveals that marketplaces have been the key driver of change (Alipay, Wechat Pay, PayPal/eBay, …). With central bank efforts (UPI/PIX) in underbanked markets as #2.

- Merchant Priorities drive reduced TAM. Merchants care MUCH MUCH MORE about acquisition and conversion than 100bps payment cost savings (blog). eCommerce is “lumpy” with Amazon, Walmart and others accounting for over 50% of the total $430B of retail eCommerce. This is why V/MA have deeply discounted interchange rates for the top 10 retailers. They pay 45-50 bps for credit and 10 bps for debit (dual routing). Placating large retailers removes A2A opportunity, eliminates potential merchant-led schemes, and creates impossible hurdles for competing schemes (ex FedNow/A2A), particularly when subtracting PayPal’s e-commerce TPV (i.e. non Venmo/b2b/xoom) – $40B A2A/RTP GDV TAM (see blog)

- Wallets are the new consumer switch (see blog). The wallet wars are largely over and w/ Google/Apple winning in US/EU and local QR schemes winning in APMEA. ApplePay gets 15bps from each card used but prefers its own AppleCard. Why would it ever let another payment instrument in the wallet? (see blog).

- A2A is not new, and consumers don’t need speed. Everything in A2A today has been tried before. PayPal has done it since 1998. Today consumers in the US pay bills in A2A through bank bill pay. They are presented with electronic remittances in formation (request to pay) and submit their payments.

- Fraud, Protections and Customer Service. Instant payment schemes have historically been regulatory-driven. As part of CNP, merchants own the fraud risk and have developed tools to manage this fraud. Because of their investment, they are well-placed to manage risk in a transaction. Within A2A, who manages the risk? What are the operating rules when there is a fraud claim? What regulatory responsibilities do banks have to research? What about rebates and returns? How is a “hold” placed on an account pending shipment and delivery of the merchandise? The head of treasury for a top 3 retailer said it this way “V/MA is the devil we know.. There is risk in any new scheme where retailers can’t define rules”. None of this rule definition has taken place.

- High costs of building a new network with no margin for a central party to guide investment. Systems complexity and dependencies on card processing (just to name a few): Customer Service, POS/Checkout, Fraud, Advertising (audience creation), Advertising measurement, data warehouse/customer data platform (CDP), treasury/cash management, processor integration, compliance, Info Sec PCI/DSS, Vendor management and DD, third party vendors. All of these costs are incurred assuming you have created a compelling value proposition and customer experience. I’m painting a picture of the investment required to make this work. The costs here create a 4-10yr payback on realizing a 100bps interchange savings.

- Aligning Incentives. Any change must create incremental incentives FOR EVERY PARTY (consumer, merchant, bank, processor, … etc.). When any of these parties see a downside risk they don’t support it. V/MA are the generic network operator that creates/enforces the rules and standards and also manages the terms of the economic model. Economics has been an afterthought of every EU-reg-driven effort. Making things mandatory (e.g. SEPA/Open Banking) doesn’t lead to revenue or investment. See blog.

- Banks are not aligned. The Top 20 banks are heavily invested in TCH’s RTP. It is 10 yrs ahead of FedNow, with Venmo and Zelle volume (disbursements) already flowing through (TCH RTP). Early Warning’s fraud data drove the success of Zelle and is also the reason why PAZE is within EWS. RTP fraud can’t be managed without these assets. Top 20 banks support FedNow from a switch/disbursement perspective, but FedNow is a bank service with each bank deciding if they want to participate, how they expose to consumers, and how to price. If customers of top 20 banks demand instant payments hey have the answer ready: Zelle.

- Bank role limitations. Banks are at neither the beginning (search/shopping) or end (checkout, service, support) of the commerce experience and suffer from a significant data disadvantage. This precludes them from creating a new products (no virtuous cycle) and connections (see Paze blog).

- Visa and Mastercard are VERY EFFICIENT NETWORKS operating on just 3-8bps. Just to restate their advantages: Ubiquitous, efficient, well-defined operating model, defined economic model, enforceable standards and certification regimes, integrated into back-end systems of all parties, … top 10 brands across all companies. Consumers TRUST these brands, this trust was earned over 35 yrs.

Where will non-card schemes find success (US/EU)?

Disbursements, recurring payments, and edge use cases (ex wallet funding).

For example, disbursements will represent 99+% of FedNow volume in the next 3 yrs (think G2P payments like social security, medicare, pension, …etc). See Fed Now Hurdles and Opportunities. With no bank set to roll out consumer facing payment initiation.

Where will TCH RTP find success? TCH RTP is already successful. The 7 largest banks are actively switching bi-lateral flows from TCH Chips (ACH) to TCH RTP (ie commercial, settlement, …etc). Disbursements are also a core focus (ex payroll). At the consumer level the core service which will drive expansion is Request for Payments (RfP), with new consumers terms out last money (see August Blog).

A2A Fintechs? Plaid, Open Banking PSPs, …? Edge UCs and consumer aggregation across banks (both very low margin). See blog

Visa Debit – US

US Banks seem to have Visa Debit in their crosshairs (see V/MA Moving Beyond Card). For those unfamiliar, Visa has over 80%+ debit market share in the US because of Mastercard’s Maestro Debit Failure (product and network). Visa has 4 key assets in Debit: 1) Card issuance, 2) Visa Debit Processing (DPS), 3) Interlink (#1 PIN debit network with 60%+ of all volume) and 4) volume agreements at merchants, processors and issuers. In short, Visa’s assets have allowed it to neutralize the impacts of Durbin on their network.

Visa Direct (and Mastercard Send) have become the ubiquitous connectivity infrastructure for FinTech’s and Neobanks (see blog) with roughly 85% of all FinTech’s investing in these services for bank connectivity. As I discussed in TCH RTP, banks have discussed the mechanics of how they can insulate bank-bank rails from V/MA network operators, particularly how they can make TCH RTP into a new debit network owned and controlled by banks.

RTP is capable of becoming the primary debit network in the US, with the underlying Vocalink infrastructure serving as such for the UK. Vocalink/RTP as the new debit network is a variation of the vision laid out by the consortium of 27 banks 13 yrs ago (under Paul Gallant).

Owning the token vault allows TCH to serve as the central routing engine for all payment types, and “see” all payment interactions (for fraud/data purposes). Today we see TCH members use RTP as their back end clearing mechanism (replacing TCH’s ACH based CHAPS) between counterparty banks that have been onboarded.

Think of it this way. The first phase of TCH volume is bank-bank settlement, next phase is commercial account to bank, then commercial account to commercial account, then adding consumers.

In a world where RTP takes on role as the new debit network, there would be no need to re-issue debit cards as a they would operate as a PIN debit (blog), consistent with Durbin routing rules. This move would also align to my 2013 view on debit network consolidation.

What is the potential impact to Visa? Minimal in 5 yr view. Banks are “stuck” with DPS hosting AND merchant-driven routing + volume agreements. Top Banks pay almost NOTHING for Visa’s interlink (given volume incentives). Thus there would be a short-term revenue hit from loss of volume incentives with no incremental revenue given the merchant’s control over debit routing. Banks COULD develop a lower cost service, but there would be additive costs as DPS could not process non-Visa volume AND incentives would be lost.

International Case Study – Brazil PIX

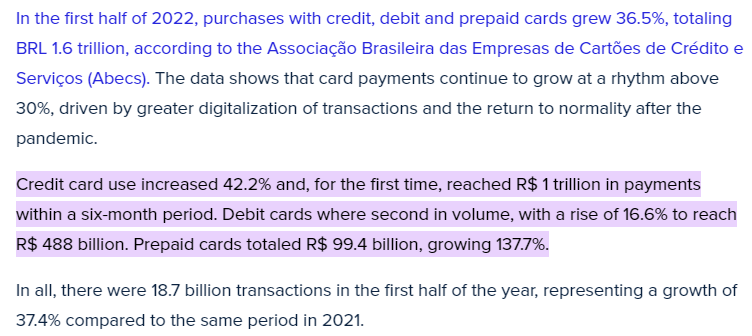

As discussed in my April PIX Brazil post, PIX is an amazing success: launched in Nov 2020 this free payment service rides on top of an instant settlement network (SPI). Brazil’s Central Bank (BCB) provides monthly reporting on PIX volumes, users and transaction types. In under 2 yrs, PIX has gone from 0 to 138.68M users (population 212M) and Volume of 1.422B $R (~$251M USD), 150.95M $R (10.6%) of which are P2B and 440.9M $R (31%) are P2P all growing at 31% CAGR (YoY Aug-Aug). The most frequent question I get from investors is why PIX is not a threat to V/MA.

This report from ACI shows that while PIX is growing at 31% CAGR, Card use increased by 42.2% (2022 YoY)! Why? Brazil was one of my 35 geographies during my short stint at City running international Retail channels for Ajay. Simply put Banks don’t want poor people in their branches. This base of the pyramid is served by PIX.. a “banking lite” that brings the cash economy into banking through mobile first. It is cash and bank barriers that PIX destroys (even more so in India w/ UPI). PIX brings people into banking AND electronic payments. A tide that lifts all boats.