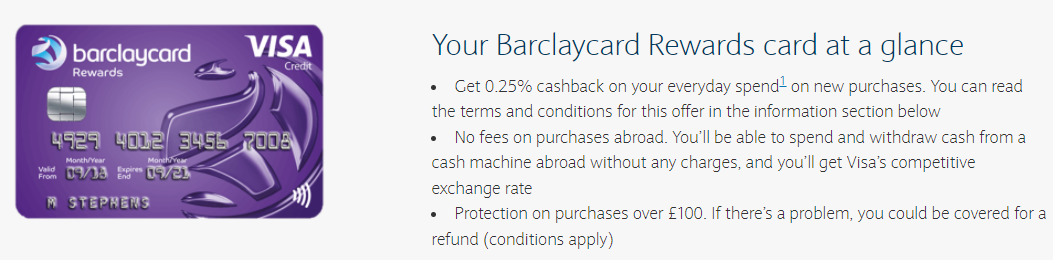

There are only 3 major markets where credit card interchange is not regulated: US, Japan and Russia. In these markets, Issuers use interchange (US 130bps-270bps) to power consumer reward programs (see Tilting Networks Toward Merchants – 2015) and card marketing. The ROW has credit interchange regulated to ~30bps and debit 20-30bps, and the reward programs are much different (Barclays UK below). But regulating payment interchange HAS NOT resulted in volume loss for V/MA, to the GREAT frustration regulators.. this is a key point (more later).

Noyes Payments Blog

Inside Baseball for Payment Geeks

5 thoughts on “Interchange is going toward 0.. So what?”