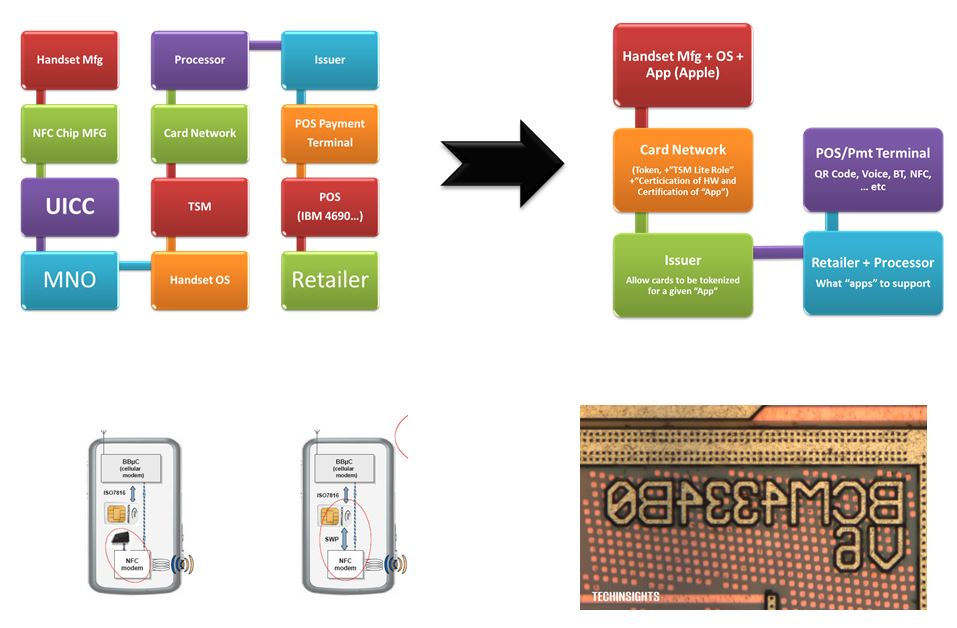

Bull Case For Visa and Mastercard

Very Long Blog. 4 Page Exec Summary. Feedback appreciated. This blog has been my “blocker” as I’ve iterated over the last 7 months. I’ve thinned this down from 31 pages (which no one would read) to 23. No I will never write something this big again.

The thoughts below are an update to my 2016 Small Wins, where I outlined how the forces that have driven scale, and shaped organizations, are atrophying (Transaction Cost Economics, asset intensity, information intensity, finance… etc). Paul Graham’s calls this change Refragmentation, I call it Transformation of Networks.

It’s as if the gravitational constant (the big G) is changing and new forces are driving the formation of new networks influenced by a rapidly evolving world of “weak links”. Information intensity has moved beyond “tweaking” 100 yr old business models to transform the design of industries, communities and people.

Whereas the 2016 blog was more about the “possibilities” enabled by tech, this blog is about the reality of how things will evolve.

© Starpoint LLP, 2024. No part of this site, blog.starpointllp.com, may be reproduced or retransmitted, in whole or in part, in any manner without the permission of the copyright owner. Also see our Legal/Disclaimer (this is a highly opinionated and partially informed blog).

You need to be logged in to view the rest of the content. Please

Log In. Not a Member?

Join Us