Sorry for the long quiet period. My youngest just graduated High School and as a WWII history buff, his gift was the Band of Brothers tour from Normandy to Salzberg. We came away with a new appreciation for the cost of freedom and the sacrifices made all of those in the armed forces.

European Payment Insights

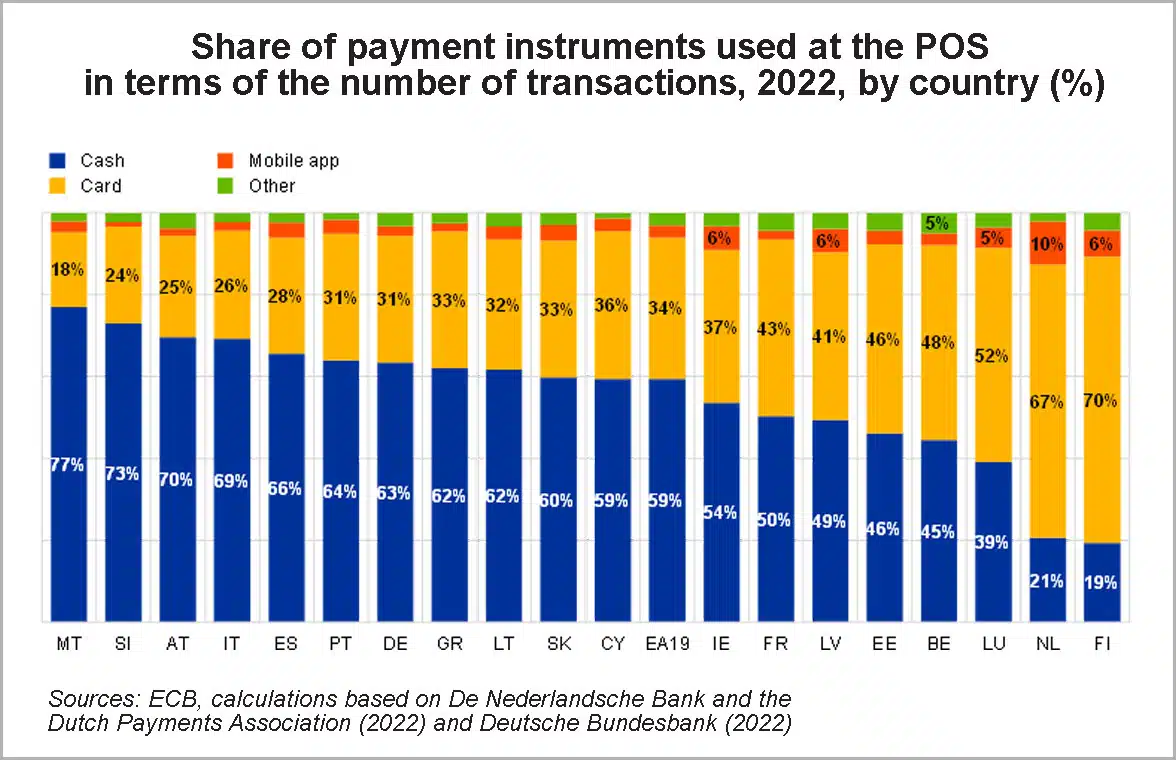

Covid had put a long pause on my travel to Europe. In the 6 countries we visited I was pleasantly surprised at the broad acceptance of contactless and tap to pay. Beyond tapping with my iPhone, most restaurants first attempted to tap cards before a “dip”. Contactless now comprises ~60% of POS transactions, a behavior 3-5 yrs more advanced than the US and certainly one of the drivers of card GDV growth in the EU. The V/MA position is Europe is perhaps stronger than in any other market, as any new scheme would also need to integrate seamlessly into this acceptance (and presentment) infrastructure.

EU Merchant – Cost of Acceptance

While the EU’s 2015 IFR brought interchange down to 0.35/0.25 the payment industry made up much of the loss on the acquiring side with new merchant fees. In Innsbruck, Salzberg, and in Venice I was consistently hit with “we can’t accept cards right now”.. “Do you have cash”? After coming to the register with $200-$500 of merchandise I would tell them “no” and begin to walk out of the store.. Only for them to say “lets give it a try”.. And it always worked. I was struck by the “coordinated denial” by all merchants in a region.

Anecdotally, small merchants related they are paying $3,000-$5,000 a month just for their merchant account. If true, Europe would seem to be ripe for the Square model which would simplify acquiring for small merchants (EU readers please feel free to comment).