Let’s talk about tokens. When discussing tokens and payments, it’s important to clarify which category of tokens you’re talking about. Today, I’m not discussing NFTs; instead, I’m discussing card network tokens. It’s hard to believe I’ve been writing on this subject for almost 15 years. For a historical refresh, here are a few of my old blogs

What are the core functions of a digital wallet and what will the future bring now that Apple has opened up their Secure Element (see blog)?

I’ve been writing about wallets for over 12 yrs. Let me recap some history

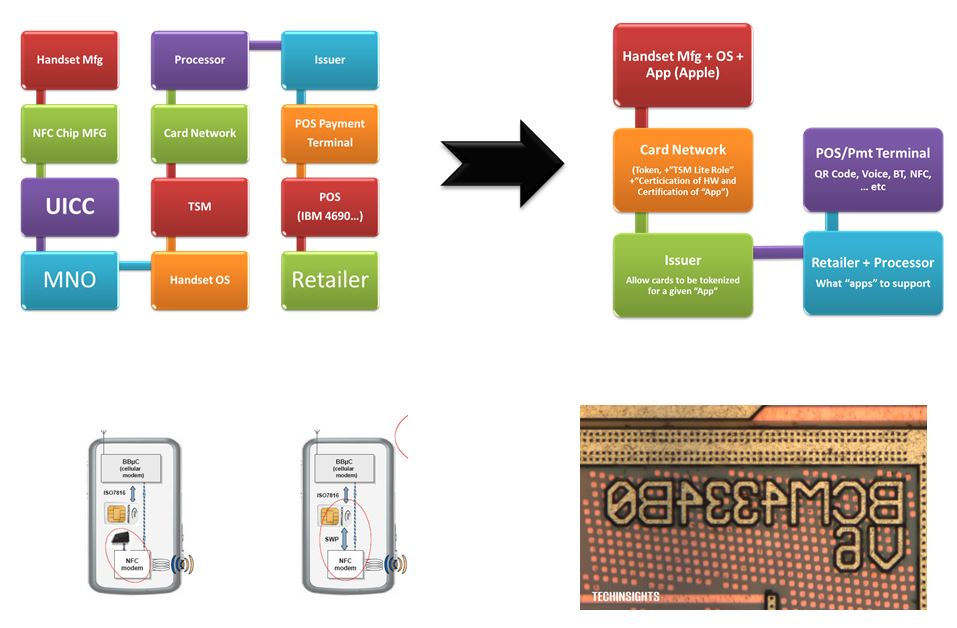

In 2006, mobile operators had control of what “apps” could operate on a phone. In the US Qualcom bought Firethorne in an effort to create a single bank application, where banks had to pay $1 for every balance request. I’m not joking.. Open app stores destroyed this model quickly, but so the MNOs pivoted to the SE and SIM card.

In 2010, Mobile Network Operators (MNOs) had control of the encryption keys for secure elements. Their pitch to Google was, “Give us a billion dollars, and we’ll give you the keys”. The absurdity here was only surpassed by Doug Bergeron (CEO of Verifone) marching into Google the next year and asking for a “Billion dollars” for Verifone to support contactless (I was just outside the meeting room). Of course there was no economic model for Google to make a single penny off of payments back then. Even worse, there were 12 parties in the NFC ecosystem, all looking for economics, yet there wasn’t a dime to share between all of them (blog). Now wrap all this silliness into a MNO consortium with the name ISIS.. yep.. What a great brand!

From 2008-2014 the GSMA had a global vision for managing the phone’s secure storage (see blog) and monetizing it for the MNOs. MNOs could control either the secure storage within the SIM card with Single Wire Protocol (SWP) or within the secure element.

ApplePay’s 2014 launch did several things that changed the game. 1) Ripped away control of the SE from MNOs and OEMs, 2) integrated payments and security into the OS (Card in SE, biometrics in Secure Enclave), 3) required a card to activate a new phone, 4) Created economics with the networks for payment (see blog).

From 2007-2014, US Issuers wanted to only enable credit cards for contactless (a premium experience). 27 Issuers (led by Citi’s Paul Galant) were working on their own wallet, to “own” mobile payments (see Civil War). In 2014 launch of ApplePay, Apple forced the Issuers to enable debit at parity to Credit, and also gave Issuers a take it or leave it revenue share (15bps in US, 7bps in EU and ROW). Charlie Sharff (then CEO of Visa) also established a fundamental network rule in “no wrapping”. You can’t wrap a Visa card with another number and let it operate. A rule that was ahead of its time and also more formerly established with Durbin regulations.

The 27 bank project thus floundered for 16 yrs until last year when saw the light of day in PAZE. Paze is Gen 5 of this effort, and really a white label version of SRC. A wallet that abandons the POS and focuses on eCom with Visa given the reigns as the lead architect only last year (see eCom Politics and Scenarios)

Today, Issuers classify Apple as “enemy number 1” because of the 15bps fee that the Issuers voluntarily signed up for. Their renewed complaint is that merchant discounts (ie 45 bps and Costco, Walmart and Target) puts them upside down on transaction economics. Apple’s position (anecdotally) is “you knew what my fee was when you gave the discounts.. You voluntarily signed the agreement.. And now its successful you want a discount”? (see 2022 US Payments Environment)

While the tech changing eCom is amazing, there are only 3 options for organizing it into a successful platform: 1) Government Led, 2) Standards Led, 3) Commercial (payment) Network. Of the 3 only V/MA have established an economic model where participants can invest (see Identity Models and my new blog this week on topic)

Wallets have grown substantially from “payments” to the consumer interaction point for “everything” between the virtual and physical world. Door keys, concert tickets, boarding passes, DLs, loyalty cards, student IDs (see Apple’s list of UC’s it will support).

ApplePay will be supported in every browser. This will be a game changer and dramatically increase payment volume flowing through Apple wallet (and their platform). Just last week, the WSJ published a great piece on why retailers hate that consumers make large purchases on their computers. Apple will expand ApplePay to support all browsers AND provide a major upgrade in experience, security and fraud.

In January of this year, Apple offered commitments to the EU to assuage their concerns about NFC payments and mobile wallets related to the EU’s Marketplace Fairness Act (MFA—see blog). Apple’s approach follows Google’s model in Host Card Emulation (HCE—see Apple Developer Doc).

Visa’s network is the largest commercial network in the world, moving over $15T in volume over 4.3B cards in over 200 countries. Visa’s core is called VisaNet, a real-time messaging network between banks. They don’t move money but send instructions to and from banks, merchants, consumers and other approved third parties. The banks move the money, primarily through net settlement on ACH. The beauty behind Visa’s network is its operating model, which allows thousands of partners to invest billions of dollars. To defeat Visa, you not only have to create a better network, but you must also create a better economic model for EVERYONE to switch, AND overcome the combined investment of all current stakeholders. This is why SEPA failed (see Power of Bank Networks).

You need to be logged in to view the rest of the content. Please Log In. Not a Member? Join Us

I see this as round 4 for Apple. The first rounds were fought with mobile operators and their GSMA TSM vision. The next with Australia (2016) then EU (2019). I find the timing of this report very interesting. As CFPB report came just months after US Issuers pushed Apple to eliminate its 15bps fee (a fee they voluntarily signed up for). I wonder if the CFPB knew that the Issuers collectively sought to eliminate the fee, or that they would like to expand PAZE to NFC/POS in order to lock a new wallet app which would DECREASE BANK COMPETITION (and cut out Apple).

You need to be logged in to view the rest of the content. Please Log In. Not a Member? Join Us

Sorry for the long quiet period. My youngest just graduated High School and as a WWII history buff, his gift was the Band of Brothers tour from Normandy to Salzberg. We came away with a new appreciation for the cost of freedom and the sacrifices made all of those in the armed forces.

European Payment Insights

Covid had put a long pause on my travel to Europe. In the 6 countries we visited I was pleasantly surprised at the broad acceptance of contactless and tap to pay. Beyond tapping with my iPhone, most restaurants first attempted to tap cards before a “dip”. Contactless now comprises ~60% of POS transactions, a behavior 3-5 yrs more advanced than the US and certainly one of the drivers of card GDV growth in the EU. The V/MA position is Europe is perhaps stronger than in any other market, as any new scheme would also need to integrate seamlessly into this acceptance (and presentment) infrastructure.

Square’s stock (aka Block) took a big jump after last week’s announcement that they would also be a partner in ApplePay’s new ability to accept payments. Today I thought I would cover what this will (likely) look like and 5 reasons why Apple Tap and Pay is a big deal.

You need to be logged in to view the rest of the content. Please Log In. Not a Member? Join Us