Short Blog

https://usa.visa.com/about-visa/newsroom/press-releases.releaseId.19621.html

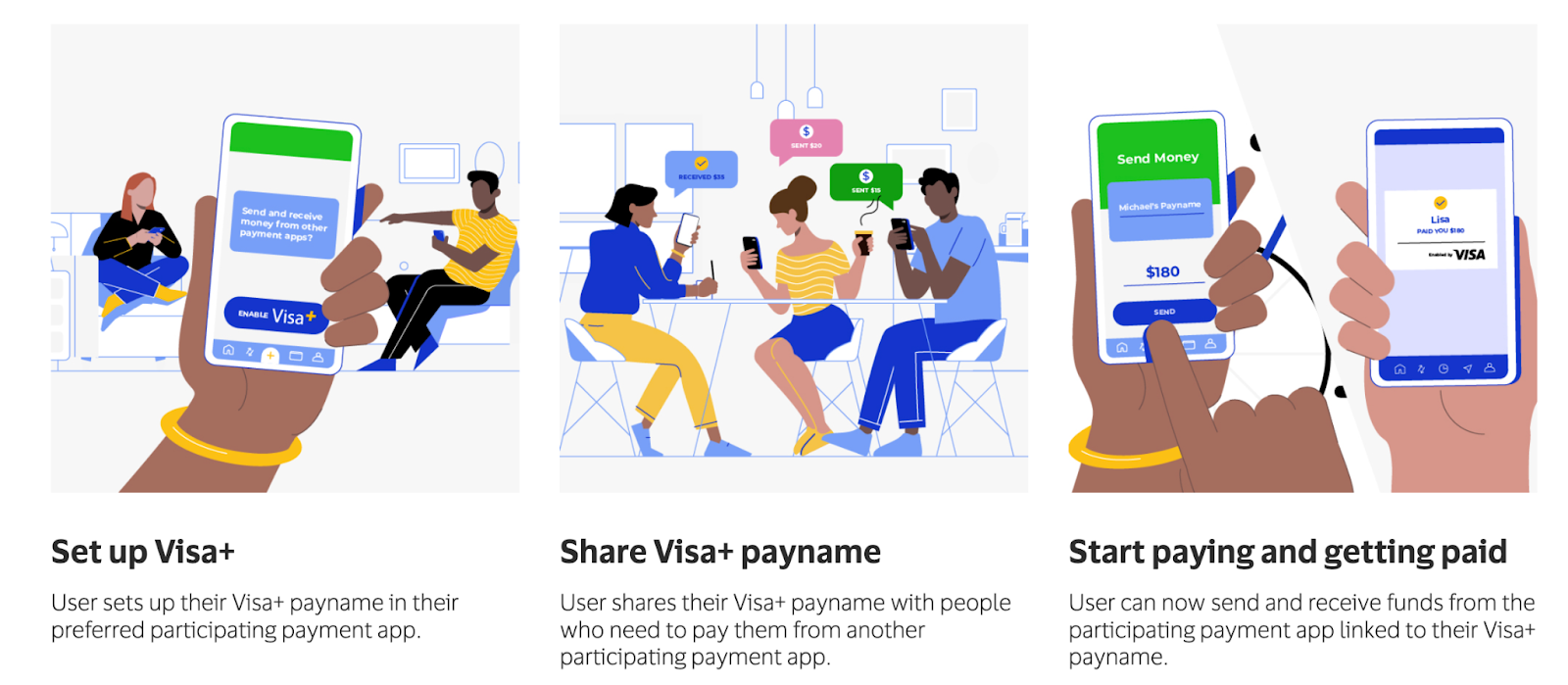

Today Visa announced a major expansion of Visa Direct called Visa +, with PayPal as the anchor launch partner. “help individuals move money quickly and securely between different person-to-person (P2P) digital payment apps” without requiring the recipient to have a Visa card.

Visa+ expands Visa’s role as the meta-directory of payments connecting consumers, wallets and accounts with a master “payname”. If I were to write the marketing one-liner for Visa+ it would be “pay people in the way they want to be paid”.

While P2P and wallet interoperability is the PR focus for the launch, disbursements may represent the largest volume

- Marketplace payouts – Small Merchants ($200B)

- International Payroll/Commissions ($400B+)

- Dividend Payments – Non-Bank International (~$50B-$100B)

- Healthcare/Insurance Disbursements

- …etc.

The case for PayPal is solid, as Visa+ interoperability allows consumers to keep their current relationship (ie wallet) and payout to any other connected wallet. It also expands the capabilities of Paypal in disbursements (ie hyperWALLET). I do wonder if Square Cash connects… P2P and perhaps allowing a SquareCash customer to pay with PayPal? LOL

Other wallets will be faced with a key decision on whether to open up their walled gardens. My guess is that they will selectively partner for interoperability cross border (where they don’t play) or for eCom (where they are not accepted). My recommendation for Visa would be to focus an Asia GTM on Visa+ as the marketplace interoperability platform. Allowing any wallet customer to pay any ecommerce merchant with the new “payname”.. AND integrate Visa’s fraud services (ie Cybersource) to drive GDV in AP eCom.

P2P Cross scheme interoperability among QR Wallets in Asia is significant, but central banks are heavily involved in wallet schemes and cross border interoperability (see effort by 5 SE Asia countries).

Economics

Page 19 of Visa’s rate table shows the pricing of Credit Transfer. Network fees and processing fees are not included here.

Visa Direct GDV growth has exceeded 44%, as I discussed in V/MA Moving Beyond Payments. While I see minimal near-term GDV (~<$2B) in cross scheme P2P wallet (ie no Zelle or SquareCash integration), I see significant disbursement volume (2%-10% Incremental Visa Direct) with a dependency on Asian Wallet integration.

More detail on the service here

Tom question – I get that for PYPL, it’s good to establish interoperability between PYPL and Venmo (though it raises eyebrows that they needed Visa to do this for them…). But that said, it seems overall potentially disastrous for many of these wallets. If you have Venmo and I have Cash App, previously I’d be incentivized to download Venmo if I wanted to pay you (i.e. the network effects of P2P apps)… now, why bother, if I can just send you $ from my Cash App wallet to your Venmo wallet?

Perhaps from PYPL’s perspective, that’s the point – maybe they figure that they already have the massive scale of users, so if this cuts off the user acquisition growth for wallets generally, that’s good for them (undermines their competitors vs. they already have the lion’s share of users).. and they don’t really make $ on P2P anyway so who cares…

But point being, if Visa is now connecting every wallet on the planet, that seems like a huge deal for Visa (positive) – and similarly a huge deal for the value prop of each individual wallet (negative). Curious for your thoughts

If every wallet were identical, performed the same service, and only made money by keeping consumers inside their walled garden, you are correct. PayPal makes money from merchant eCom (380 bps). Allowing any card, ACH or 3rd party wallet to access that makes sense for them. Your Square Cash UC is the one I’ve been thinking about. SQCash is much more like a bank, with high crypto user base. SQCash has merchant acceptance play only on square merchants (90% POS). There could be a play where you could register SQCash as a payment instrument in PayPal.. they both would win in this structure.

Your point on wide open interconnection is valid. Smaller wallets would want the connection as they grow, to demonstrate ability to use. Think of Europe where PayPal is the #1 eCom payment method (Germany, France, …etc). Allowing wallets to pay with PayPal would help all of them.. as well as PayPal.

Cross border is another win.. while Asia has central banks making bi-lateral agreements in QR wallets, most countries do not. The card metaphor provides XB revenue upside for wallet.

In summary, connections to PayPal make sense because of their merchant acceptance take rate. Connections between two similar wallets in the same market don’t seem to be likely..