I’m usually just a cynic. Today, I’m constructive with specific suggestions for PayPal’s new executive team. Note that about 80% of your large institutional investors will read this..

Exec Summary

- Wallets are a core battlefield for Issuers, BigTech, marketplaces, and governments.

- PayPal’s previous “super app” strategy failed because there was no clear consumer value proposition.

- The most significant consumer value proposition to be unlocked is the unbundling of financial services, with the wallet providing the common UI to manage the complexity. In this future state, a “super wallet” would enable bank competition for every account and every transaction.

- PayPal is well positioned to execute on a super wallet, but it must go ALL IN on a consumer-focused value proposition without regard for issuer relationships.

- For example, Curve is the best-in-class Wallet providing aggregation, transaction, loyalty and analytics across all account types, networks, POS, eCom, P2P and banking services.

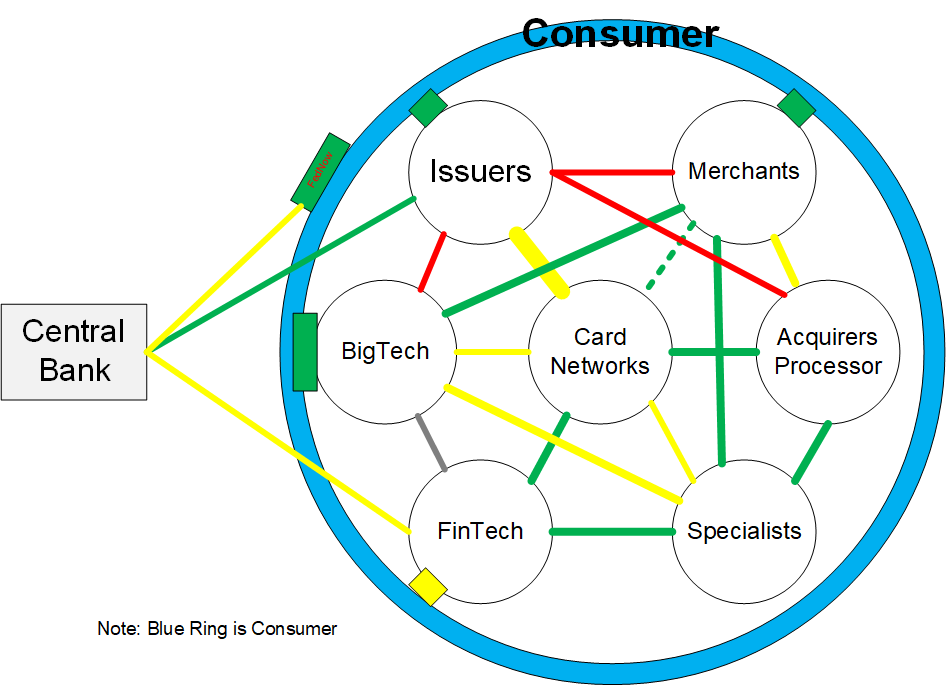

Payment Network Effects & Innovation – Quick Recap

Payments are hard to change once network effects take hold. As I laid out previously in Innovation in Networks

- Each stakeholder has invested in joining the network, from merchants (payment terminals, gateways and fraud-fighting services) to issuers (acquiring the customer, issuing the card), …etc.

- Consumer behavior becomes ingrained.

- Maintaining multiple options is expensive as there is limited “energy” in maintaining numerous alternatives.

- Bank, Consumer, Merchant and Platform connections become ubiquitous

- Large entities operate at superior economics (see blog) and have a vested interest in maintaining the status quo (Issuers and Merchants)

- New networks are focused on 1) low end, where there are poor margins; 2) high end, where there are multiple alternatives; or 3) Specialty flows (government, healthcare, supply chain, …etc).

This resilience is exemplified in V/MA EU volume post-Interchange Fee Regulation (IFR – 2015) and PSD2 (i.e., Open Banking). To the dismay of the Nobel Economists, efforts to eliminate “excess profits” (see Nobel Economist Jean Triole) have impaired competing schemes from creating value (i.e., competing), further entrenching V/MA. See Power of Bank Networks

Figure – Tom’s Ugly Payment Network Map – Discussed in US Payments – Where to Invest

As scale increases, change WITHIN a network becomes more complex, as change for one party has implications for all those connecting. While sustaining innovation (ex, fraud, identity) takes place within the network, disruptive innovation finds a new operating model, such as

- New networks (ie PAZE, SEPA, UPI, RTP, FedNow, …etc.)

- New bundles

- Merchant – Toast, Shift4, ShopPay, …etc

- Consumer – Wallets, Affirm, Square Cash, ApplePay, Curve

- Vertical – Supply Chain, Healthcare, Government Disbursements, Financial Markets

- Orchestrator/Marketplace – Google, Amazon, Facebook, Alipay

- Central Bank/Regulatory – UPI, PIX, SEPA

- Standards Driven – Blockchain, Web3, DeFi, ….etc

- New Consumer Front End (THE WALLET)

For V/MA, we covered this topic in Innovation in Networks, and for Google/Apple in Wallets, Trust and APIs. But what about PayPal?

PayPal – Efforts to Transform Beyond ‘the Button

PayPal had a vision of becoming the OS for Commerce, but has failed at this in three distinct times. First, in 2001, the dot-com bubble burst, leading to a significant downturn in the tech industry. PayPal was not immune to this economic crisis and was forced to adjust its business strategy. With Amazon, Banks and others bidding, PayPal eventually sold to eBay, which provided it with a much-needed boost in customer base and transactions. As I’ve mentioned before, marketplaces and top merchants have proven to be the #1 source of new payment types (Alipay, AmazonPay, RedCard, …etc). eCom volume blossomed, but PayPal became lazy; it was like getting wet under a waterfall.

The company attempted to expand its reach into the brick-and-mortar retail space in its second iteration. After the disastrous launch of an organic plastic card (See 2012 blog PayPal’s New Plastic – a card running on Discover). They appointed Dan Schulman as the new CEO in 2014. Part of Dan’s mission was also to complete the spin out from eBay. Dan and I went out to lunch in NY the Friday before he started. We both recognized that PayPal needed to evolve beyond its core business of online payments to remain competitive. He set out to transform PayPal into a more comprehensive financial services company, offering its customers a wider range of products and services.

“We see an explosion of marketplaces,” said Bill Ready, PayPal’s chief operating officer, in an interview. “We want to serve them with a full operating system for commerce.” – Bill Ready COO Paypal – WSJ.

PayPal made a number of acquisitions in its quest, with 2 standing out: Braintree and hyperWALLET. Bill told me the platform was revolving around three cores. Braintree for marketplaces and payment acceptance, hyperWALLET for payout and legacy core PayPal. While Venmo is a consumer success, it has always lacked revenue (Braintree acquired Venmo in a firesale for ~$10M as they couldn’t make payroll).

With all-star Payment Exec Bill Ready putting together the plan and the major pieces acquired, things looked quite promising in 2018. Unfortunately, Dan broke a tremendous promise he made to Bill. Something like, “I’m only in this for five years, then it’s yours”. You can imagine Bill’s surprise to see Dan’s new CEO contract and stock deal come across his desk in 2019 (as COO he had to sign off on regulatory filings)… all without a phone call. Bill’s departure to Google in 2019 (exactly 5 yrs after Dan’s first term) was an insurmountable loss for PayPal. Who was left to create a unifying product vision? No one (we got a super app instead).

2019 was a time of tremendous turmoil, with Bill leaving and eBay selecting Adyen just a few months prior in 2018. Institutional investors wanted to know the plan. I told Dan that if he wanted to compete with Adyen, he needed a complete refresh of his exec team. From the comfy CEOs that he made wealthy through acquisitions. To enterprise software experts. He needed to look much more like Oracle and SAP than he did a consumer products company. He needed to have leaders who were hungry to make a change—not waiting for their earnouts. Post 2019, PayPal’s strategy has been all over the place, from an attempted $45 billion acquisition of Pinterest (2021 blog), SuperApp (2019 blog), and Bank for the Unbanked to Venmo QR at the POS. These efforts went nowhere. Without a compelling product vision, the components within PayPal are a millstone of distraction and waste. Braintree is killing it, but the Branded Paypal ‘Button’/Wallet is losing share. How can they recover?

PayPal – Consumer Innovation Opportunities

Readers know I’m quite optimistic about the prospect for Wallets to lead in innovation as they are the primary consumer interface (see How will eCom evolve?, Wallets becoming the next Platform); PayPal is the OG wallet, but losing consumer traction quickly as they become a Braintree company – a commoditised merchant acquirer. For those that don’t follow, the analysts BT is delivering ~30% growth, and branded payments are losing market share (primarily to Google, Apple and SquareCash). I covered PayPal’s existing plan in Shock to the World, which was shocking. Moreover, PayPal is expected to see further headwinds with the increasing footprints of checkout products such as Shopify, Payz, and Visa/Mastercard “Click to Pay”.

What does PayPal need to do to innovate with consumers? While V/MA have thousands of issuers, merchants, and specialists investing in their network, PayPal is a three-party network (like Amex and Discover), while this gives them flexibility in rule setting, there are very few external parties investing in PayPal’s network to expand or improve its operation (see Changing Economics of Payments).

The pragmatist in me sees six key innovation vectors

- Change the competitive dynamic (ex enable bank competition)

- Expand Merchant End Points (ex POS)

- Expand Domain (ex Banking, Advertising)

- Expand Consumer Interaction (ex Identity, “Bank Lite”, Crypto, Super rewards …etc.)

- Sustaining – Reduce Friction and Increase Conversions

- Enable Partners (3rd party investment in PayPal’s network)

But the big picture “theorist” in me asks, “how can PayPal change the competitive payment dynamic?

What is fundamentally broken? Or to “what is the problem to be solved” (Clayton Christensen Innovators Dilemma)? These innovation vectors mean NOTHING if they are not part of a compelling consumer value proposition.

Going ALL IN on the Consumer – a ‘SUPER WALLET’

What would a maniacal focus on the consumer look like? An “All in” strategy where there is no concern over bank “partnerships” or “merchant value”. What services do consumers need to manage their financial lives across all accounts? With one interface on mobile. A “super wallet” that seeks to help customers find the best financial services provider, fostering competition for every element of their business and helping them navigate all their interactions. This would be the opposite of Sandy Weill’s financial supermarket, the UNBUNDLING of banking.

Example: As Yodlee’s first banking customer in 1998, my Wachovia team realized great consumer value in providing an “integrated view “ across all account types. We provided cross-account analytics, but we didn’t provide much in the way of “action” or recommendations. Also, see Google Wallet and Plex.

As outlined in FUTURE OF RETAIL BANKING, market forces are broken in retail banking, with the largest banks growing much larger in their own virtuous cycle. A Super Walet would be a strong force for competition by enabling consumers to manage the complexity of many providers, each of which competes on rates and service for every transaction. It would leverage combined data across your portfolio, integrated analytics and a community to suggest the best accounts/approach. If there were better services available, it would assist them in instantly opening new accounts (with either banks or FinTechs).

Now you see why banks are frightened by non-bank wallets. Banks would love to be the fox guarding the hen house to reduce competitive dynamics and retain the key interface and control point. Google, Apple, and others see the value of wallet beyond banking and payment. For example, Wallets and identity are also needed in other domains: Government Services and Credentials, Healthcare, Education, Travel, Entertainment, Physical Access Controls, …etc

Product Features of a Super Wallet

A SUPER WALLET must manage all of your accounts in a common interface. Yes, this was the early vision of Google Plex, but it was also what Intuit and Microsoft did in the PFM days and Mint does today—my list of Example Features.

- Common Interface across all account types.

- Beyond Aggregation to Action – Alerts to action, payment and transfer execution, optimation of cost/interest or loyalty, taxable event tracking, scenario planning, analytics

- Manage Identity and Bank Terms/Agreements

- Hold data locally under consumer control. From bank data to receipts, warranties, and terms.

- Cash Management – Break transactions between credit and current accounts

- Provider Management and Tracking – Enable bank competition for both credit and deposits. Quickly switching balances and purchases to the best provider

- eCommerce and POS

- Operate across all payment types, card, RTP, A2A, P2P, Crypto

- Quickly evaluate merchant BNPL offers against other financing opportunities

- Alerts for changes in rates, with AI suggesting alternatives

- Integrated reporting across all financial relationships

- Integrated rewards schemes across account types, with options to optimize rewards

- Authorization and Identity/password management across account types

- Fraud and identity alerts

- Asset/stock tracking and NFTs

PayPal’s Strengths Aligned to the Opportunity

PayPal’s “Super App” strategy of 2019 conflated banking, payments, and lending. It was more of a consistent UI for PayPal’s numerous acquisitions than it was “super” at anything (see blog). There was no well-defined consumer value proposition. The result was an abject failure.

To be clear, I’m not trying to recast the Super App. Rather, a SuperWallet is a MANDATE TO go “all in” on a consumer value proposition. Fortunately, PayPal is THE BEST PLACED company to lead this, and their imperative is no longer masked by COVID volume growth as they now have a significant loss of branded share (consumer side of their network – see blog).

PayPal’s unique assets

- 400M global customers and over 150M in the US.

- Wallet Apps in both Android and iOS

- MSB/EFI licenses globally

- BillMeLater/PayPal Credit

- 20 yrs of unique risk/fraud data (see blog)

- Integrated Card and Non-Card accounts

- Negotiated rates for credit, debit, ACH

- Integration to Plaid for Instant Account Opening

- Seasoned Engineering Team

- Venmo P2P

- Payment Form Factors from QR to NFC

- Open Banking Integration in Europe

- PSP Operations

- Compliance

- Global Operations with local Data Residency

- …etc

Example Super Wallet – CURVE

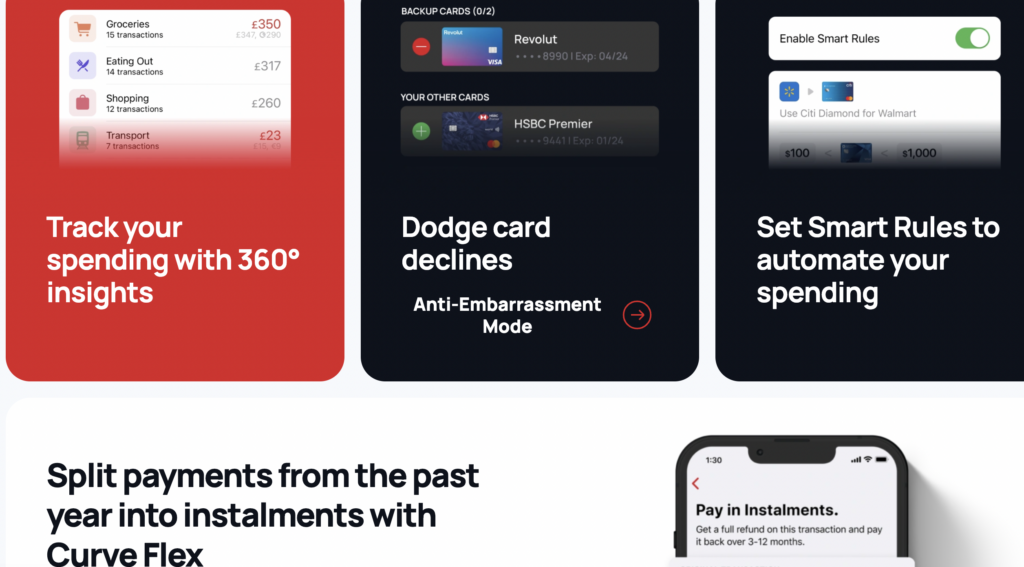

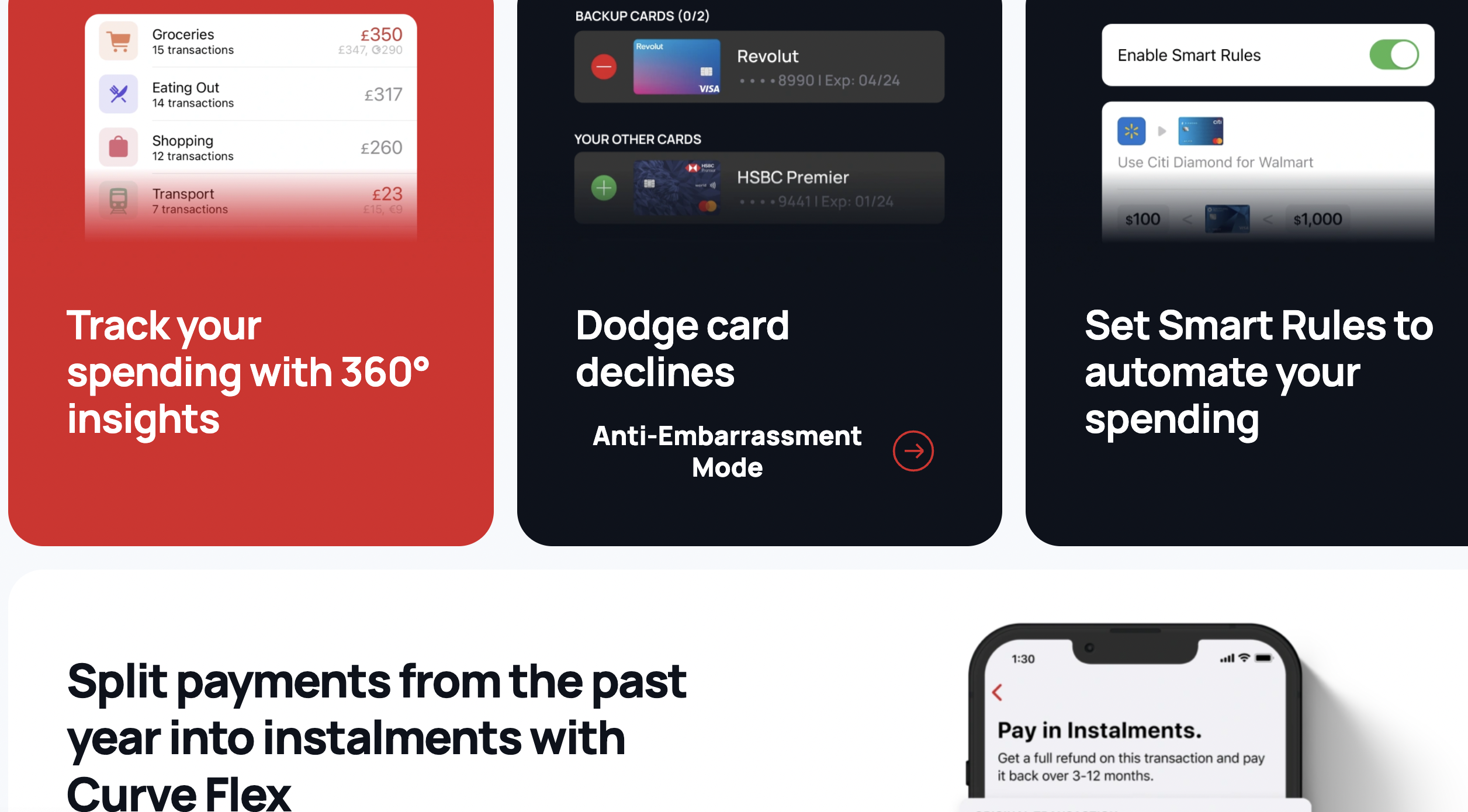

What would a super wallet look like? How could PYPL leverage its assets to execute an “All In” consumer strategy? The best Super Wallet I’ve found in the market today is Curve. I’ve been using it for four months now, and it is groundbreaking in 6 core elements

- Mobile CX. Just amazing. As a reminder, my view is informed by running bank channels for both Citi and Wachovia

- Action and Transaction. Smart Rules for Transaction Routing across account types and splitting transactions

- Aggregation and Analytics leveraging Open Banking Integrated Loyalty across all account types

- eCommerce and POS wallet on par with ApplePay

- Network agreements allowing back-back transactions

- Customer satisfaction and growth.

While Curve started as a Google Wallet-like card that wrapped other cards, it has dramatically expanded. Today, Curve integrates into most financial account types, enabling actions across payment rails. On Android, it delivers contactless payments (through HCE) for Samsung+ and others. It is also likely to be the first wallet on iOS to provide contactless payments (see EU MFA Apple Agreement).

Key Point – While PayPal is a three-party network, Braintree’s growth is as a processor for V/MA (4 party networks). PayPal must change direction away from building a bespoke POS acceptance and realize that it is more important to serve the consumer across financial products and external networks than creating your own (product or network). The WALLET is MORE IMPORTANT than the network. If you own the wallet, you can steer and clear (as PayPal did 15 yrs ago).

From my perspective, Curve is making excellent progress toward building the OS for money by immersing itself in its customers’ financial lives.

A Wallet that enables bank competition.

Short Postscript

I’m fortunate to have been around many visionaries in this space during my Citi team’s acquisition of Egg in 2007, Yodlee’s first customer, and as the #1 PFM bank at Wachovia (02-06).