Fraud, Trust and Real Time

4

Today’s blog is part 2 to my 2016 post Transaction Costs and Value Orchestration in Commercial Networks. The “Big Picture” questions I’m trying to answer today are:

Will Visa Acceptance Cloud (VAC) be a watershed event that simplifies merchant acceptance and embedding payments into iOT? Changing the merchant side of the network has been a nightmare for all. VAC enables a radical expansion of merchant network capacity with one big asterisk. (Sorry for Typos)

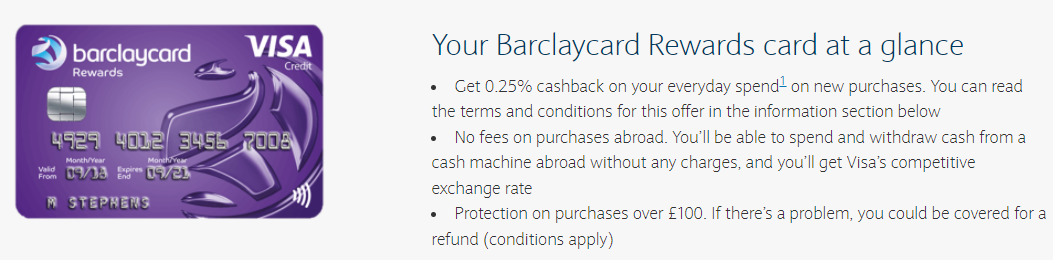

There are only 3 major markets where credit card interchange is not regulated: US, Japan and Russia. In these markets, Issuers use interchange (US 130bps-270bps) to power consumer reward programs (see Tilting Networks Toward Merchants – 2015) and card marketing. The ROW has credit interchange regulated to ~30bps and debit 20-30bps, and the reward programs are much different (Barclays UK below). But regulating payment interchange HAS NOT resulted in volume loss for V/MA, to the GREAT frustration regulators.. this is a key point (more later).

My perspective has been evolving as I work to build out infrastructure for “when Crypto grows up” in my new Company. I’m pleased to report that Accept Payments (acc3pt.com) went live this month and is expanding our private rollout as we fine tune all of the CX. Thought for the day… Its about trust..

Very short Blog – Recapping a few tweet streams.

I think FedNow is a great effort to provide an open alternative to TCH’s RTP. I’ve spoken with, and consulted for, the KC fed on a number of occasions and provided my input to the FedNow service back in 2013. Per my blog last week the survey result from the Fed’s efforts found “emergency bill payment” as the top consumer use. Paying someone faster brings on risk. The Fed depends on banks to manage risk and price that risk. As a former banker running payments at 2 of the largest banks I have a view here.

Sorry for typos

My good friend Dave Birch wrote a piece in Forbes today on Account to Account transfer threat to V/MA. I wanted to provide an alternate view. This will likely be a multi part blog.. today I’m starting with the consumer and the merchant (from a US perspective).