BIG Changes to NFC: Payments Part of the OS

2

10 Jan 2013

NFC is a beautiful technology with uses far beyond payment. In the payment use case however, it is not the technology, but rather a business battle over control and ownership (a 12 Party NFC Supply Chain Mess) which has conspired to create many forces against NFC’s payment success.

As I stated yesterday, latest news is that MCX has chosen QR code based approach from Gemalto (following Starbucks success). My guess is that Gemalto has developed a one time use QR code that is derived from device information (it will change for every transaction… ). You can safely assume that ACH will be the primary funding mechanism (just as in Target’s Redcard and Safeway’s FastForward). The banks had some idea of MCX’s plans are thus moving aggressively to create a directory service to “protect” customer DDA information via tokenization. My guess is that this protection will come at a price….

Here is my best guess of the transaction flow (assuming the rumor is true).

Registration

Usage

I like QR codes for their ubiquity and established consumer behavior (thank Starbucks in the US). Stores don’t need to buy any new hardware for this to work, there is a zero cost of issuance, and it will work on a broad spectrum of phones. Development cycles for Store POS software are normally 18 months… so it could be some time before we see something come out.

QR codes may not be rocket science, but NFC has demonstrated the downside of tech heavy solutions. We may not need a $400M F22 when a simple bicycle will do. Carriers face a future as dumb pipes, a future share by banks, as both work to control their market positions instead of delivering value. MNOs and Banks (in the US) have proven themselves equally incapable of succeeding with new walled garden strategies. Commerce will find the path of least resistance, like a mighty river…

The big challenge for MCX will NOT be in technology, but rather a consumer value proposition. Retailers stated goal is to bring death to merchant funded bank card reward programs. What will convince me to part with my Amex card at the POS?… it will need to be something substantial.

Another often asked question is can MCX keep a bunch of fierce competitors working together in the same tent? This approach seems broad enough to insulate MCX from retail competitive forces and align them in fighting a common enemy. Per Sun Tzu “the enemy of my enemy is my friend”. Retailers are looking to turn the tables on the 2% “payment tax” on their business. There is serious enterprise commitment to making MCX work, banks will do well to treat them with respect.

Who will lose in this approach?

Other Related Blogs

2 January 2013 (updated typos and added content on kyc, cloud, and push payments)

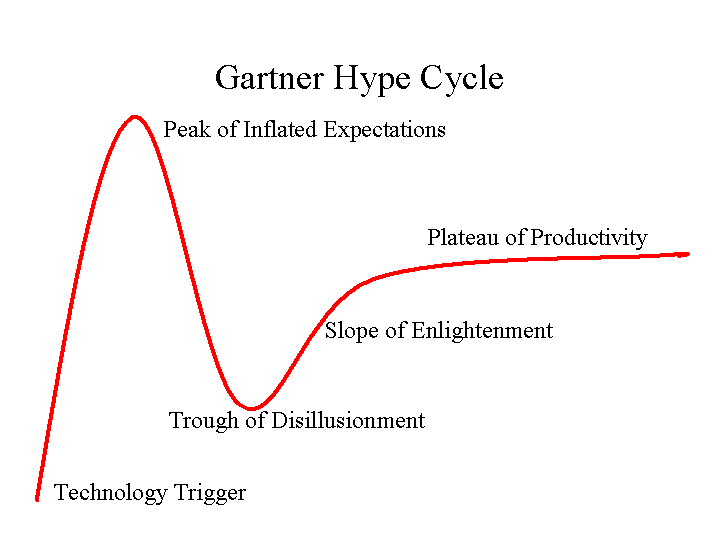

Looking back to my first “prediction” installment 2 years ago, 2011: Rough Start for Mobile Payments, not much has changed. Although I am personally approaching the “trough of disillusionment”. Lessons below are not exclusively payment (ie mobile, commerce, advertising) but seem relevant .. so I mashed them together. Key lessons learned for the industry this year:

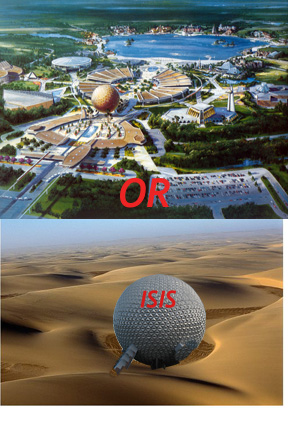

without a compelling value proposition…) and we have our current state (see my Disney in a desert pic). Take a look at who is executing today and you will see product focus around a defined value proposition. My leaders: Square, Amex, Amazon, Sofort, Samsung, Apple, SKT, Docomo and Google. Organizations can’t continue to stick with leaders that are focused solely on strategy, or technology, or corporate development… You should be able to lock any 3 people in a room for a week and see a prototype product. The lack of depth in most organizations is just astounding. Executives need to bring focus.

without a compelling value proposition…) and we have our current state (see my Disney in a desert pic). Take a look at who is executing today and you will see product focus around a defined value proposition. My leaders: Square, Amex, Amazon, Sofort, Samsung, Apple, SKT, Docomo and Google. Organizations can’t continue to stick with leaders that are focused solely on strategy, or technology, or corporate development… You should be able to lock any 3 people in a room for a week and see a prototype product. The lack of depth in most organizations is just astounding. Executives need to bring focus.Predictions

Here are mine, would greatly appreciate any comments or additions.

As I wrote in a previous note Banks will win in Payment: But which ones? Banks are very well positioned to execute. They have the consumer relationship, the merchant relationship, the IT infrastructure, and have always taken a key role in “commerce”. However, Banks have tended to operate in a slow “evolutionary” model.. and are now in a very dangerous position. Their network is complex and brittle, their value proposition and brands diminished, and the value equation has shifted.

If you are a bank and looking to “optimize” your approach to mobile payments, what are your key assets and constraints?

As a bank, would you invest in NFC? A standard owned by the card groups, and telecos and despised by retailers? Of course not.. it does nothing to help banks, merchants or consumers…

The centerpiece of any Retail Bank strategy should be to protect the consumer relationship. If you “blew up” payments today and started from scratch, how would you redesign it? I agree with Ross Anderson (See KC Fed) Ross Anderson “If you solve the authentication problem.. everything else is just accounting ..” . Why should I pass my credentials to a merchant, processor, acquirer, network, .. all just to give them to my (issuing/originating) bank? Why on earth would I pass around real account numbers (ex Checks)? Why do all these entities get to see me? What if I could interact with the originating bank directly to instruct them to send the payment?

We have seen “credit push” attempted globally with Sofort, SMS Pay, NACHA Credit Push, SEPA Credit Transfers, UK Direct Credits, US Trials with Padiant,…etc. All have a “mixed” record of success, with the biggest issue being consumer adoption and margin/bank incentives. Given US Bank recognition of the innovation problem with 4 party networks, and the need to consolidate debit processing, it would seem there is some movement in furthering this model in the US.

Unfortunately, the trials with Padiant have been a flop. A specialized payment terminal creates unique QR code which is captured by a payors phone camera. Phone sends to code to acquiring bank. Processor looks up consumers bank in directory and sends to originating bank for consumer auth/approval. Funds are then PUSHED directly to merchant and terminal gets auth. Top issue is consumer phone data connectivity, and a rather complex user process. Of course this is a starting point, and can be improved.. retailers just needs to get the buyer a few critical pieces of info:

I like this “Push model” MUCH.. After all I can push the payment from either a debit or credit account. The merchant need not know, and consumers remain anonymous throughout the transaction. Push takes almost all fraud out of the system and keeps authentication with the entity that KYC’d the consumer (the originating Bank). It gives the Banks tremendous flexibility in constructing new focused solutions at POS, eCom and mCom. Heck, its also aligned with Apple’s QR code wallet. The perspective will feed my update on Part 2 of Directory Battle.

For investors, impact is as follows

As a side note, I recommend the reading of Visa’s Debit Defense Strategy

www.digitaltransactions.net/public/frontend/files/0207net.doc

2 Nov 2012

Android Police published a story on Google’s forthcoming plastic pilot yesterday.

What do we know? Very little beyond the photo above.. If the story does pan out, it could be a tremendous win for retailers, consumers and even banks. The only loosers? NFC and carrier led payment initiatives.

Solution overview:

Business Strategy Changes

My guess is that Google will proceed with a small scale pilot, just as it did with Wallet 1.0.

Why do retailers win? (see related blog)

Google will be in a position to drive the lowest cost payment (perhaps better than 0bps MDR) AND allow retailers to drive marketing to their consumers online and via mobile.

Why do consumers win?

With Google, use any card you want, use any phone you want … consumers get to CHOOSE. (In ISIS the only card you can load today is a Visa credit card)

More to come this weekend.

Google sorry that some idiot spoiled your release plans.. but this is super stuff… I always wanted a black card.

My biggest questions?

26 Oct 2012

Today when you use iTunes, PayPal, Amazon or Google wallet do you think about which card in the back end your purchase will go on? Most of us take the view that “it just works”, and perhaps ensure that the default card is the one which allows you to accumulate the most points (Amex for me). When eCommerce started, there were few entities capable of managing card not present (CNP) risk hence specialists evolved (PayPal, Cybersource, GSI, …) that could manage this risk on behalf of the merchant/community. Payment cards/accounts had to be wrapped by these risk specialists in order for payments to be processed. As mCommerce evolved (think Apple iTunes), digital goods purchases where integrated into the “platforms” to allow seemless purchasing of content… thus starting the process by which cards were associated with “cloud” accounts accessed in mobile phones. Today, mCommerce sales are around $170B in the US, and mCommerce sales are around $10B (Digital Goods ~$4B and physical the rest .. which includes buying from Amazon on your iPad at home). Quite frankly card companies

about which card in the back end your purchase will go on? Most of us take the view that “it just works”, and perhaps ensure that the default card is the one which allows you to accumulate the most points (Amex for me). When eCommerce started, there were few entities capable of managing card not present (CNP) risk hence specialists evolved (PayPal, Cybersource, GSI, …) that could manage this risk on behalf of the merchant/community. Payment cards/accounts had to be wrapped by these risk specialists in order for payments to be processed. As mCommerce evolved (think Apple iTunes), digital goods purchases where integrated into the “platforms” to allow seemless purchasing of content… thus starting the process by which cards were associated with “cloud” accounts accessed in mobile phones. Today, mCommerce sales are around $170B in the US, and mCommerce sales are around $10B (Digital Goods ~$4B and physical the rest .. which includes buying from Amazon on your iPad at home). Quite frankly card companies  didn’t mind letting other entities like Amazon and Apple store your card information so that you could buy in either the eCommerce or mCommerce markets…. This is all changing for physical commerce because the PRIZE IS BIGGER.

didn’t mind letting other entities like Amazon and Apple store your card information so that you could buy in either the eCommerce or mCommerce markets…. This is all changing for physical commerce because the PRIZE IS BIGGER.

With the Physical POS sales $2.4T (USA not including T&E, Auto, Oil/Gas)… The established networks and banks are saying “don’t wrap me”:

All of these wallets (Virtual, NFC, Cloud, …) are causing issuers to wonder “who is top of wallet”?.. and how does a customer select my plastic. They seem much more concerned about one physical plastic card wrapping them (ie Serve and Paypal) than a virtual wallet, but they are also very concerned about data and letting any ONE intermediary see transaction data (and add offers/services on top of them). In other words “DON’T WRAP ME” (see blog Paypal at POS). Of course there is not much to worry about yet. Paypal is reportedly doing less than 5 transactions per WEEK per Store at HomeDepot.. But the established players want to stop anything before it starts.

How do cloud wallets manifest themselves? Well it could be NFC/Paypass, physical plastic, a QR code, or a voice print (Square).. all you need is a form of authentication (see Battle of the Cloud). Add to this the complexity of retailer data, issuer pricing, loyalty and incentives and the market is just nuts. Who is doing what to whom…? its like a 70s drug and sex movie.