What are the strategic drivers of change?

Where are the profit pools and how will they disperse?

A Maturing Landscape, A Shifting Playbook

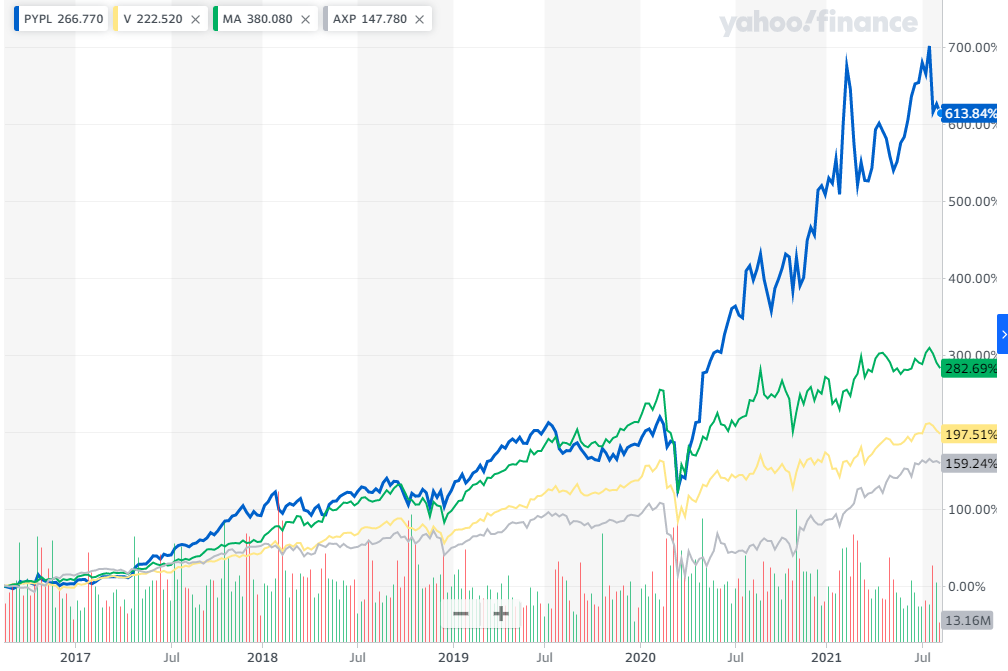

Retail payments have been a cornerstone of growth and shareholder returns for decades, delivering TSRs that rivaled the tech sector. But this golden era of easy expansion is fading. Today, growth is slowing and investors are refocusing on unit economics, distinguishing between platforms with SaaS-like predictability and those more exposed to the vicissitudes of consumer credit, deposit spreads, and regulation (see Cap Gemini World Payments Report)..

This change in tone isn’t just financial, it’s structural. Value creation is migrating away from volume and into experience, infrastructure, and intelligence.