Having just completed a merchant survey, Retail CMOs were quite clear with their top 3 companies they would spend time with to improve eCommerce (payment focus):

Continue readingGoogle Payments – Why they will Win – Globally

Reply

Having just completed a merchant survey, Retail CMOs were quite clear with their top 3 companies they would spend time with to improve eCommerce (payment focus):

Continue readingAn update to my Data Games – 2021

© Starpoint LLP, 2025. No part of this site, blog.starpointllp.com, may be reproduced or retransmitted in whole or in part in any manner without the permission of the copyright owner.

Electronic receipts (eReceipts) COULD transform the retail landscape by offering numerous benefits to consumers and businesses. With the potential to enhance digital wallets, improve customer experiences, empower AI agents, and increase advertising effectiveness. However, the widespread adoption and sharing SKU-level data face several challenges, most of which are NOT technical. Today, I’m providing an overview of key business and economic challenges of unlocking SKU data.

Keeping up with the latest in agentic commerce, artificial intelligence (AI), payments, and data privacy is an ongoing challenge. Data and LLM are the key ingredients fueling the rapid advancements in AI and machine learning innovations. As a privacy advocate, I remain deeply concerned about the centralization of data. Once AI models are built to understand “you,” they no longer need continuous access to your data—just ongoing observation (see blogs on Data Centralization and Payments and the Observer Effect).

Do I think wallets will become “Agents”? No, but they will be the most important interface to all Agents, as they broker identity, authentication, authorization, permissions and highly secure data in the handset. My view is that Wallets enable many agents. This view of the the world is called the Agentic Mesh where specialized agents work together to achieve a result.

I’m on a brief vacation celebrating my 28th anniversary and deep in thought (pic below). What am I thinking of here on the beach? Wallets, Networks, Trust and Privacy.

As digital identities continue to evolve, one of the most important debates centers around who controls and operates the wallet that holds these identities. Specifically, should wallets be separated from authorities that legally issue “identity”—commonly known as Identity Providers (IdPs)? This issue is particularly relevant in countries like India and Europe, where digital identity initiatives have made significant strides, yet their approaches raise important questions about privacy and control.

Continue readingStimulating community discussion is the #1 reason I write this blog. The intersection of payments, banking, and technology is evolving rapidly, and I’m fortunate to engage with great minds like Dave Birch and new friends like Simon Taylor. Dave’s recent post on crypto predictions got me thinking about a topic I keep coming back to—wallets and networks.

As a former banker, I’m naturally more skeptical about FinTechs disrupting the core of banking. Consumer behavior is incredibly difficult to change, and financial services are among the most competitive industries in the world. If there’s one concept where my perspective diverges from many thought leaders, it’s the power of bank networks (read more). These networks are the foundation of financial transactions, and they continue to define the way money moves.

© Starpoint LLP, 2025. No part of this site, blog.starpointllp.com, may be reproduced or retransmitted, in whole or in part, in any manner without the permission of the copyright owner. Also, see our Legal/Disclaimer (this is a highly opinionated and partially informed blog).

My estimates for how US eCom market share will shift in next 3 yrs are at the end of this blog.

eCommerce is not a single monolithic market. There are many “segments” to optimize that vary by geography, retailer type, consumer device, customer type (guest vs loyal), transaction type (recurring vs new), ad type, payment type,…etc. A great source of this information is Monetate (highly recommend). For example, let’s look at conversion rates by industry, device and region.

Continue readingAs we wrap up 2024, I thought I’d outline a few key areas I’m tracking and things to look for in 2025.

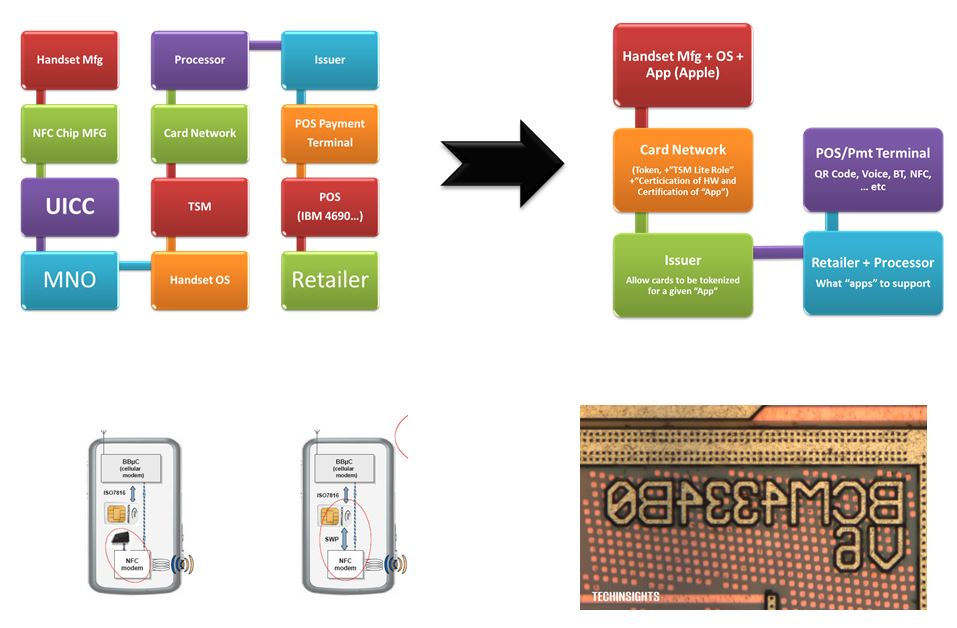

Continue readingWhat are the core functions of a digital wallet and what will the future bring now that Apple has opened up their Secure Element (see blog)?

I’ve been writing about wallets for over 12 yrs. Let me recap some history

Apple Opens NFC. Just off the phone with Apple. They were nice enough to treat me as a journalist and I was able to ask a few questions.

Read First – Blog on SPA from Checkout.com

Background Reading – June blog eCom politics and Scenarios, and Identity, Authentication and Risk

What’s the big news here? SPA allows Google to stand at par with ApplePay in providing the best-authenticated checkout experience. Google looks to have taken TWO MASSIVE pieces out of the authentication process: 1) 3DS handshake (putitting in Cryptogram and 2) A step up from the Issuer (possibly – a significant portion of this blog). This is a generational improvement and massive simplificaiton of the current 3DS flow.

The mobile platform is key to authentication and Google is the preferred partner of every bank, merchant and network. Their challenge in SPA? Doesn’t seem Checkout.com coordinated with the networks on SPA (ie liability shift OR step up). I think it will get worked out as the quality of this innovation is just fantastic.

As I wrote in June, ApplePay 2.0 plans to cross the chasm from mobile only to desktop (as announced at WWDC). Google is proving that they have the same capability, as Chrome makes up about 10-12% of eCom and over 30% of guest checkout at most retailers; they are positioned well (particularly in Android markets).

Continue readingNotifications