27 March 2012

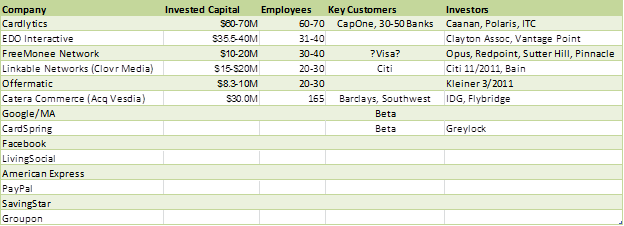

We see in the press that Google/MA have gone beta with Card Linked Offers, and Bank of America is about to go live with “BankAmeriDeals”. I last gave an overview of this space back in November in my Card Linked Offers post. For those that haven’t seen it, there is also a must read blog by Reed Hoffman in Forbes on the subject: The Card is the new App Platform.

Here is my blog from 3+ yrs ago – Googlization of Financial Services – outlining data flow. My purpose is mentioning this blog is not to show how smart I am (as an alternate view is already firmly established), but rather to highlight how much my view on the opportunity has changed over the last 3.5 years. As I tell all of the 12 start ups in the CLO space.. if Visa couldn’t get this to work what makes you think that it will be easy for anyone else.

There is a CORE business problem I didn’t realize back then.. merchants don’t like cards and are VERY reluctant to create ANY unique content (offers) where card redemption is REQUIRED. Further constraining the “capabilities” of CLO is lack of item detail information within the purchase transaction. IBM is the POS for 80% of the worlds to 30 retailers. Take a look at the 4690 overview here, notice what incentive solution is integrated? This was a 5 yr project for Zavers…

A story to illustrate my point on retailer reluctance. As most of you know POS manufactures like IBM, Micros, NCR, Aloha are implementing POS integration solutions similar to what Zavers has done. Most of the CLO companies above are paying the POS manufactures to write an “adapter” that will work within their POS and communicate basket detail information. (ISIS is rumored to have a 200 page Spec for this POS integration as well). There is a very big difference between having integration capability, and a RETAILERS agreeing to use it (ie share data). There must be a business value proposition for retailers to move… and I can tell you with a great deal of certainty.. Retailers don’t like the BANK card platform.

I emphasize BANK for a reason.. I was with the CMOs of 3 large retailers a few months ago. When asked what their payment preferences where, they answered without hesitation: Store Card. This is their most profitable product used by their most loyal customers (think private label). Do you think for a moment that a Retailer would deliver “incentives” to customers that are not in this group.. Remember, these PVL loyal customers also hold a number of other bank cards, and there is not much in the way of customer matching between data sets. I think you get my point.

As I stated previously, all offers businesses are highly dependent on targeting. Targeting is dependent on customer data, relevant content, effective distribution (SMS, e-mail, an App), campaign management (A/B testing, offer type, target audience, …). Campaign management is very dependent on feedback. There are very few companies that can effectively TARGET and DISTRIBUTE. The current group of CLOs is partnering with the banks to solve the targeting problem (example Catera/Citi, Cardlytics/BAC, …). This is further EXASERBATING the poor Retail adoption. Why? Here is what a CMO told me:

“Tom, lets say a consumer just shops at Nordstrom.. the card network and bank see that I just completed the transaction and now market to them … the advert is “go to Macy’s and save 20% on your next purchase”… Given that they can only offer basket level incentives this is how it must work… Tom do you know what will happen? The customer will return what they just bought and go to Macy’s and get it. How is this good for Retail?”

From an Ad Targeting/Distribution perspective, Mobile Operators certainly have an eye on this ball (mobile phone). But only a few companies like Placecast can actually deliver it for them. MNOs are truly messed up in this marketing space (within the US). If you had the CEOs of Verizon, ATT and ISIS in a room and asked “who owns mobile advertising”?.. ISIS would say nothing if both of the other CEOs were in the room.. They want it.. but no one will give it to them as they can’t execute with what they have in this space. Verizon would say “many partners”… Their preference would be to sell the platform akin to their $550M search sale to Microsoft in 2009. So VZ wants a $1B+ Ad platform sale… who would compete for that business? I digress.. but what is in place today looks much more like a rev share… Internationally there are carriers with their act together: Telefonica and SingTel (just bought Admobi).

Let me end this CLO diatribe with a customer experience view. Let’s assume I have 12 CLO players.. each partnered with a different bank/network. Also assume that all are heavily dependent on e-mail distribution. I have 6 different cards.. and will be getting at least 6 e-mails per week with basket level discounts. Now assuming that I can keep track of which offer was tied to which card.. and use the card. I’m still left at the POS with a receipt that shows none of these basket level discounts (as they are “credited” to my account after purchase).

Without POS integration AND Retail data sharing this will not work.. the customer experience is terrible, as is the campaign’s restriction on basket level discounts. The ubiquity of cards is attractive.. as is bank data on Consumer “Store preferences”…. But both work to the detriment of retailers. What consumers will see in CLO for some time is the generic 10-20% off your next purchase that will also be available in direct mail campaigns… Let’s just hope that someone can work the double redemption problem…

My read on this for Google is a little different. Google is positioning itself as a neutral platform.. it can do Retailer Friendly.. Bank Friendly… MNO Friendly.. Manufacturer Friendly… Each will have different adoption dynamics. Google’s objectives are likely: gain insight, be the central platform for marketing spend, be the most effective distributor of content, … . This offer beta would certainly seem to be a “bone” thrown to banks.. hey… here it is … good luck trying to make it work.