PayPal under attack.. Not just Facebook…

16

29 August 2012

29 August 2012

Previous Blog – Part 1 – May 11, 2012

Let’s update the Cloud Battle story and discuss events since my last post on the subject

Square, Visa, Google, PayPal, Apple, Banks, … have recognized the absurdity of storing your payment instruments in multiple locations. All of us understand the online implications, Amazon’s One Click makes everything so easy for us when you don’t have to enter your payment and ship to information. (V.me is centered around this online experience). Paypal does the same thing on eBay, Apple on iTunes, Rakutan , …etc. But what few understand is the implication for the physical payment world. This is what I was attempting to highlight with PayPal’s new plastic rolled out last week (see PayPal blog, and Target RedCard). If all of your payment information is stored in the cloud, then all that is needed at the POS is authentication of identity (see blog).

The implications for cloud based payment at the POS are significant because the entity which leads THE DIRECTORY will have a significant consumer advantage, and will therefore also lead the breakdown of existing networks and subsequent growth of new “specialized” entities. For example, I firmly believe new entities will develop that shift “payment” revenue from merchant borne interchange to incentives

Since May, the following “significant” events “in the battle” have occurred:

Where are the cloud battle lines? Well most significantly the battle lines are forming away from NFC (as I stated in January). Even my old friends at Gartner have caught up and placed NFC in the trough of disillusionment. To restate, NFC is not bad technology.. but it delivers no “value” in itself beyond control. Mobile operators have consistently failed to build a business around a “control” strategy (see my Walled Garden Blog). In the ISIS example they mandated use of credit cards only, as this higher credit interchange was the only way to make revenue. Well guess who pays the freight here? Yep the merchants… Wal-Mart and its peers were not thrilled at giving issuers and MNOs 3.5% of sales for the privilege of accepting a mobile payment.

The Cloud battle is complex, as the strategies are about MUCH MORE THAN PAYMENT. Payment is the ubiquitous service that is the last phase of a successful marketing, engagement, shopping, selection, deliver, retention, loyalty process. Leaders from my vantage point:

Payment Networks:

Physical POS:

eCommerce/mCommerce:

How many places do you want to store your payment credentials? Who do you trust to keep them? What data do you want providers to know about you?

From a macro economic perspective, total payment revenue for all major participants is just under $200B in the US. Total marketing spend in the US is over $750B. Total retail sales in the US is $2.37T (not including oil/gas, Fin services, T&E). Marketing is fundamentally broken… payments is not. Retail sales gross margin has been compressed from 4.2% in 2006 to 2.4% in 2010. Who is best able to execute on the combined retail and marketing pain points? Who can be retailer friendly? Consumer friendly? Marketing friendly?

I start my analysis with #1 the consumer value proposition, and #2 the merchant value proposition. Entities like Google, Paypal, Apple already have tremendous consumer relationships and traction. They thus have very few “acquisition” costs. However, these entities do bear the costs of changing customer behavior. There are many approaches for changing customer behavior:

Other groups like MCX and ISIS bear the cost of both customer “acquisition” AND behavior change for: Consumer, Merchant or Both. As I state previously. one of my favorite arcane books I’ve ever read was “Weak Links” I’m almost reluctant to recommend it because it is so good you may jump ahead of me on some of my investment hypothesis. One my favorite quotes from the book

Scale-free distribution (completely open networks) is not always the optimal solution to the requirement of cost efficiency. .. in small world networks, building and maintaining links between network elements requires energy…. [in a world with limited resources] a transition will occur toward a star network [pg 75] where one of a very few mega hubs will dominate the whole system. The star network resembles dictatorships in social networks.

Networks like V, MA, PayPal, Amex and DFS are working to participate in this new Macro economic opportunity. But established networks are hard to change

“The network forms around a function and other entities are attracted to this network (affinity) because of the function of both the central orchestrator and the other participants. Of course we all know this as the definition of Network Effects. Obviously every network must deliver value to at least 2 participants. Networks resist change because of this value exchange within the current network structure, in proportion to their size and activity.”

The implications for cloud based payment at the POS are significant because the entity which leads THE DIRECTORY will have a significant consumer advantage, and will therefore also lead the breakdown of existing networks and subsequent growth of new “specialized” entities. For example, I firmly believe new entities will develop that shift “payment” revenue from merchant borne interchange to incentives (new digital coupons).

The current chaos will abate when an entity delivers a substantial value proposition that attracts a critical mass of participants. Today most mobile solutions are just replacing a card form factor… this is NOT VALUE. I am currently placing my bets on solutions that merchants support (Square, Google, MCX, LevelUp, …) as this is a key “fault” of almost every other initiative.

Comments Appreciated (as always sorry for the typos…)

3 Aug 2012

Paypal COULD do everything that Google wallet does today.. so why won’t they? (Note I’m talking about the Physical POS… not online)

I’ve had a PayPal debit MasterCard for 6 yrs, when I use it at any merchant PayPal deducts from any stored balance I have, and then hits one of my stored payment instruments. I use this card exclusively on international trips because they have always offered the best cross border fees (.. and just 3 years ago paid an interest rate higher than any of my banks). I looked on the back of my new PayPal debit card and see that JP Morgan Chase is the issuing bank. Given that Chase has over $10B in assets, this card costs the merchant $0.21 + 5bps in the US. This is a great deal for retailers. A REALLY great deal.

Why is PayPal pushing out its own Plastic? Unbranded? Obviously they really don’t like the standard debit interchange (above) and want a bigger cut (than $0.21 flat fee) from the retailer. (see PayPal at POS)

Why won’t PayPal expand its online wallet to allow me to select any card for any given purchase? In this I mean creating an app that works like Google wallet, prompting the customer “what card do you want to use”? The answer is that they want to drive the underlying account selection decision to ensure the instrument with the lowest cost is selected.

Take a look at your payment instruments in PayPal today, they let you define a DDA account as “primary” but NOT a card. In other words PayPal incents you to link DDA in order to get money out.. then PayPal looks to leverage this account whenever possible (sometimes taking take settlement risk). The most costly customer for PayPal would be an Amex customer with no linked DDA and a PayPal debit card (for ATM withdrawals). See my related blog on PayPal’s funding mix (estimate 150bps)

PayPal is a payments business.. not an advertising business. Their goal is to maximize revenue. This is not a bad thing… But their recent moves are a “replay” of what happened to the bank payment networks as they pushed to ramp up merchant fees and grow interchange revenue at the expense of retailers. Why on earth would any merchant agree to take on Paypal’s new plastic? If it is above $0.21 it makes no sense at all… UNLESS Paypal is driving incremental sales.

PayPal today could create a Virtual “wallet” tied to either a Sticker or a Card that would work across Android, iOS, Blackberry, … and do everything that Google has done.. Why won’t they? Because the instrument must operate as a debit card, and the interchange “arbitrage” could kill them. In other words they will bear the cost of 350bps for a CNP Amex transaction and only charge the merchant $0.21 flat fee. If they rolled this out, I’m sure they would have MASSIVE success.. but if customers unlink DDAs and delete debit cards they would risk a funding mix that is “unsustainable” because they have no other revenue channel.

The true “payment innovation” from Google has little to do with payment and much to do about risk management and monetization of data. Google drives business to retailers today.. google helps consumers find the right product… they also “know you” from your history. They can use this information drive value to consumers AND to retailers.. they are also willing to take a very big risk that the benefits of Google will out weigh the COSTS of WALLET. Google Wallet will likely loose money on every single transaction. If you never accept an offer, incentive or coupon.. never search.. never use maps to find a business, never use Zagat to find a restaurant, never watch you tube commercials… they will likely loose money on you. However Merchants will ALWAYS win.. no matter what, they will have the lowest cost payment when accepting a Google payment.

This is either INNOVATION OR INSANITY. From my perspective, what Osama and team have done is fundamentally game changing.. ! Bearing costs, giving consumers and retailers complete control.. in the hope that they can deliver value in other services. Payment is now just a small part of an overall Commerce Process. For example, a “new” feature of Google Wallet that has not received enough attention is the “saveto” API release at Google I/O . Google allows merchants to store 3rd party offers and payment types in the wallet. These offers don’t have to be created by Google.. it is a true “wallet” function.

As I stated yesterday, Visa, Mastercard, Amex, all of the banks are REALLY worried about data. Google will be in a position to deliver value to consumers independent (or dependent) on the card you use. Few other companies can do this… Consumers will always have a choice.. no one will be forcing them to use their Google wallet. But why not? Why didn’t the banks use their information to help me earlier? Why did the banks and payment networks stop retailers from passing their real costs along, of delivering incentives that they could control?

This “aggregate” model is something ANY company could do in short order.. Square is doing it, Revolution Money, LevelUp, … but no one else can make it profitable.

PayPal’s new POS “hope” is to re-engineer the customer experience at the POS, allow merchants to throw away their custom POS terminals.. As most of you know I believe Square Register was by far the best POS experience I have ever seen. From PayPal’s June Video it looks like they agree and have replicated the Square Register “voice” experience. While the customer experience is FANTASTIC.. it did not bring the customer into the store.. nor is payment cost competitive with Google.

[youtube=http://www.youtube.com/watch?feature=player_profilepage&v=CMByV-k9Oc4]

Investment take

PayPal has enormous runway left for them globally. I don’t see Google wallet denting current growth for 2 years. However this is VERY disruptive. IF google is successful in getting all Android users to register with a payment instrument (like Apple does in the App Store), and Google pushes Wallet out beyond NFC phones, it could result in a Tsunami wave which Paypal could not overcome in mCommerce.. This is a scenario where there are 3 primary mCommerce payments options: Apple Passbook, Google Wallet and Amazon. For physical commerce.. nothing will impact this world in next 5 yrs if it does not entail a physical plastic card. NFC phones and payment terminals just aren’t materializing fast enough. IF google creates physical plastic.. watch out… In this scenario Google should be pursuing an unbranded card.. “let the consumer decide”.. .”let the retailer influence” these are themes not heard in the payment world and would seem to resonate.

![]()

No Mastercard Logo on this one…

Quite impressed that they have pulled this together.. a new card network…

This is more than a decoupled debit.. although PayPal could choose to assume settlement risk through either ACH, stored debit card (or even ATM??). Paypal has the facilities to provide lending via BillMeLater (previous post) or to a consumer’s other preferred lender (via stored card). They are completely in control of a much larger value proposition as well.. with integrated rewards and a 3 party financial network that will compete with Discover and Amex.

I’m very, very impressed.. this is a new product that could completely disrupt traditional credit cards. Not only in rewards, coupons and incentives.. but in interest rates for every single purchase. This could be the only card you carry.. Forget about the “pay by phone number”.. the product innovation here is much more interesting than how it is delivered (plastic, phone number, bump, …).

Paypal also has a new site (beta) a few screen shots of which are below.

This new plastic is currently only accepted at Home Depot. My understanding it that Chase Payment Tech will be a lead acquirer for this new Product… I’m sure Vantive, FirstData … et.al will not be far behind. I will attempt a more thoughtful analysis later… thoughts appreciated.

Warning.. I ramble a bit in this one.

23 March 2012

Does anyone remember Microsoft Wallet circa 1997 (See Wikipedia)? Digital wallets are certainly not a new phenomena. Today we are struck with eWallet saturation: Google Wallet, ISIS Wallet, Visa Wallet, iTunes accounts, Amazon Accounts, Square, PayPal, … How many places must store all of my credentials?

Does anyone remember Microsoft Wallet circa 1997 (See Wikipedia)? Digital wallets are certainly not a new phenomena. Today we are struck with eWallet saturation: Google Wallet, ISIS Wallet, Visa Wallet, iTunes accounts, Amazon Accounts, Square, PayPal, … How many places must store all of my credentials?

For my own benefit I thought I would take a brief look at the history to determine what the future may look like (As the future holds the key for my investment decisions). With respect to Wallets, what are they? What are successes and why? What is the consumer value proposition? What are the risks? What does the future hold?

My last blogs on this topic were in November 2009, Investors Guide to Mobile Money, and in 2011 – Tough Start for Mobile Payments.

What is a Digital Wallet?

My all time favorite YouTube video definition is below (Courtesy of Google)

http://www.youtube.com/watch?v=gKGptWtzeaU

[youtube=http://www.youtube.com/watch?v=gKGptWtzeaU]

Proposed Definition: A consumer owned and controlled account that can store any electronic form of what is normally held in a physical wallet, including: payment, ID, coupons, loyalty, access cards, business cards, receipts, keys, passwords, shopping lists, …etc.

This definition sounds broad enough..

As a consumer, what would you think of having multiple physical wallets? I personally don’t have that many people I trust. Trust is a very important element to a consumer. Some of the information in my wallet is sensitive, and there is also a financial risk associated with loss of payment information (particularly outside of the US). What kind of entity would want to assume the risk of holding all of this information? Which reminds me of a story,

I was in a Board Meeting with a senior partner of a “Top 3” VC discussing consolidated sign on. A start up was proposing to hold all of the login credentials for all of your bank accounts. As the former internet head for both Wachovia and Citi I had some firm views on the topic and asked “who is going to take the risk if credentials are compromised”? I further explained “it is not a technology problem, but a risk problem.. Bank’s will not let someone keep their Customer’s keys if they can’t insure the risk”. As a side note, I also instituted a policy that if a customer discloses their credentials to anyone, they are responsible for any losses that result (sorry Yodlee).

Within a Digital Wallet, securing information AND giving Consumers the exclusive ability to control what is shared with whom is a challenge (beyond technology and trust). We thus have many limited “Wallets” that are constructed around specific purposes, for example Microsoft’s wallet has evolved to LiveID. From a pure technology perspective, the mobile phone (with NFC) seems to present an opportunity to provide the Consumer with a device that can uniquely handle the security and authorization aspects of a holistic digital wallet. In my view, the challenges faced by the “phone as wallet” are business related. Per my definition above, a wallet should allow consumers to control what goes in and how it is used. Today we see the carriers (ex ISIS) create a platform based upon their control, allowing only cards that have paid a fee to enter into their wallet. I digress…

What makes for a successful wallet?

Customer Trust, Customer Control, Convenience, Ubiquity (opposite of lock in), Intuitiveness, Experience in Use (buying, redeeming, accessing, ..), Security,

If I have a wallet that only accepts 3 cards that are not accepted at any of the top 20 retailers (ie ISIS), it is of little value. Why not let consumers control what goes in? This is where carriers must get to in order for NFC to survive. Even then, NFC phones are far from my recommendation. After all if your payment information is locked in a mobile phone how do you use it when you are at your computer buying something on Amazon? Locking information in a phone is just plain stupid in the age of the cloud.. most agree that individuals should have a their information in a cloud they control. The NFC zealots reading this blog will respond that it NFC doesn’t require a network and is more reliable… my response, the POS and payment terminals are connected.. NFC doesn’t need to hold the card in the SE.. it just needs some sort of identifier.. or in the Square cardcase example no NFC at all just your voice print. After all if there is no auth from the payment network.. the transaction will not happen.. so something is connected in 99%+ of card transactions.

Consumer Value Proposition

My primary digital wallet is Amazon, with Paypal as a close #2. The buying experiences are just superb, unfortunately neither extend well into the POS. I have a PayPal debit card I use here.. but I have a hard time justifying why I would use a paypal debit card that pulls money from a pre-funded account which is tied to my Bank of America Checking.. why not just use my BAC Debit Card? I don’t think I’m alone here.. The thought that comes to mind: why do I use PayPal at all? Convenience is certainly a key element, but I also really don’t like giving out all of my personal information to every vendor I do business with. Why does any vendor need to know my name? Is there a business case for anonymity? For Readers in Germany I know your answer… of course there is.

My primary digital wallet is Amazon, with Paypal as a close #2. The buying experiences are just superb, unfortunately neither extend well into the POS. I have a PayPal debit card I use here.. but I have a hard time justifying why I would use a paypal debit card that pulls money from a pre-funded account which is tied to my Bank of America Checking.. why not just use my BAC Debit Card? I don’t think I’m alone here.. The thought that comes to mind: why do I use PayPal at all? Convenience is certainly a key element, but I also really don’t like giving out all of my personal information to every vendor I do business with. Why does any vendor need to know my name? Is there a business case for anonymity? For Readers in Germany I know your answer… of course there is.

Most Silicon Valley eWallet business cases are being built around data sharing and “closing the loop”. In a network analysis model, every step away from the optimal consumer experience (control, anonymity, ubiquity,..) impacts broad based adoption. Alternatively, new value propositions (ex incentives, rewards, loyalty, …) can reverse entropy, but only within specific groups/clusters (that realize the value). Thus a highly fragmented world of wallets, each built around specific functions limited to narrow networks, where customers exercise only limited control and hence participate in a limited fashion.

Risks

My last blog on Payment Risk was associated with Square (I still don’t like the swipe, but I have eaten my shoe now that they have surpassed $4B GDV and have developed CardCase… which I love). Microsoft had grand visions for Wallet and Passport, and pulled back for a number of reasons. Globally, most consumers still have problems putting all of their information in one place. The Fed, OCC, FTC, CPFB, Banks have all been circling around the broad proliferation of consumer data.. what are the risks of having your payment instrument stored with 100s of vendors? While at the The Clearing House’s annual event, I was pinged by a JPM Chase exec.. what will be done to secure payment information? At the policy level, many believe there is a national security risk in the compromise of our payment systems… It is something all of the Banks are thinking about.

While cloud based storage of information sounds fantastic… there remains a gap in integrated controls, security and authentication. This is where I see both the US and EU taking action on consumer data access and controls much beyond what is now within PCI. Given today’s technology, there is little reason for any merchant to hold your actual credit card number.. yet it is still the case.

What business incentive is there for any entity to hold “unlimited” sensitive consumer information? If the information cannot be accessed without user consent? All of these factors will shape wallet functionality to either something focused within a given domain, or under complete control of the Consumer.

Wallet Strategies

1) Consumer Friendly.. Single store for all consumer information. Payment, loyalty, reciepts, … The players I see here are Google, Square. (note I acknowledge everyone at PayPal just rolled their eyes and point them to my Disclaimer above). Business case is around customer data access.

2) Marketplace focused. Obvious players here: Starbucks, Rakutan, Amazon, Apple, Paypal, Target Red Card. Objective: Deliver a fantastic customer experience in purchasing within a focused marketplace.

3) Form Factor/Device Focused. Mobile Operators, Card Networks, . Deliver technology and incent buyers/retailers to participate. This is not working out so well, exception is Edy.. may work in markets with dominant carrier.

4) Bank Consortium. We see this more in Europe at the moment, but I believe the US regulatory bodies are pushing banks to work together here. Much more payment focused, and thus minimal consumer value… Banks/Fed must realize mobile is not about a new form factor, but a new value network.

5) Retail/Transit Consortium. Transit is already clear leader here in Asia…. Transit actually resembles more of #2. Where there is only one transit company provider I believe it is.. this Category is defined as one wallet working across multiple retailers.. I look at this as incentives tied to something like a decoupled debit.

6) Commercial. Example outbound payments, payroll distribution, global dividend payments – hyperWALLET.

7) Other???

Future of Wallets

“Limited Wallets” can obviously be very successful: Starbucks, PayPal, Amazon, Apple iTunes, Oyster, Edy, Suica, Octopus, hyperWallet…. But all started around an existing marketplace/system. In order for an independent wallet to thrive it must deliver value within a core network. My approach to evaluating retail payments evolves around a central hypothesis: payments support a commercial system, they are only the last phase of a long marketing, incentive, shopping, selection, and buying process.

Networks are resilient to change, this is both an asset and a hindrance. The value that is delivered within an existing payment network is tied to the commercial system in which it operates. This includes both business agreements AND technology, neither of which are easy to change. As the nature of retail changes (example payments, and incentives across virtual and physical channels) new “value exchange” networks will form. Existing payment networks will certainly attempt to change, but given their distributed ownership, nodal control over rules, and legacy infrastructure it will be “a challenge”.

In the US today, this is what is happening with Google Wallet, Bank initiatives to form “the next Visa” and Large US retailer’s plans to form a new payment network that they control. Today’s wallet initiatives are operating in a very dynamic landscape: retail is changing, technology is changing, new value networks are forming, new marketing platforms are emerging.. The margin is always better in orchestrating the interaction, than in coordinating the transaction. Thus I place my “wallet” bets in the short term with groups that can control the commercial marketplace (ie Apple, Amazon, eBay, Retailers, … ), and with groups that can orchestrate new value propositions (ie. Google, Square, hyperWallet, ..etc).

Have a great weekend… My Asia thoughts are next.

10 Jan 2012

Historically I’ve been a big PayPal fan, and still am. I have a PayPal Debit card that I used this morning… and use PP every chance I get online. The online checkout process is just fantastic. In the good old days I earned more money from my PayPal money market then I did from my bank (savings and DDA), so my preference was always to keep a balance with them. Sadly this is no longer the case.

In my last post on PayPal (PayPal at the POS – Nov 18, 2011) I described PayPal’s challenges at the physical POS:

PayPal has no tools in its shed to deliver incremental value within a PHYSICAL commerce orchestration role.

There are few “payment problems” at the POS. For example, how often do you go to Home Depot and forget your wallet? Or go home empty handed because Home Depot wouldn’t accept your form of payment? Payment in and of itself is only the last phase of a long: product, marketing, retailing, pricing, selection, distribution and delivery buying process. Most retailers strongly believe that the cost of this last “payment” process has been disproportionately high relative to the value it brings. This is the key strategic battle being fought today in “mobile payments”. Banks and the card networks are trying their best to make “mobile payment” a premium service tied to 300bps+ cards… while retailers and manufactures are looking for solutions that will enable them to create new buying experiences. PayPal’s solution may bridge this transaction cost gap (blended rate), but does very little to address the physical buying process.

In the virtual world eBay is the lead orchestrator in this process (on its marketplace), as is Amazon. Key to Amazon’s and eBay’s ability to serve, as virtual world orchestrators, are their ability to control the buying process (end-end) AND the data.

However in the physical world, the buying process is highly fragmented. The value that PayPal brings to Home Depot today is based upon their current product capabilities (payment + ?) and customer base (100M+ globally). If you were running store operations at Home Depot, what are you trying to accomplish with PayPal?

I’m fortunate to have led teams at Oracle and 41st Parameter (a KP start up) that worked with some of the World’s largest Retailers (online and physical)….. It is based on this perspective that I see the following business issues with PayPal-Home Depot approach:

1. Incentive to use payment instrument. As a consumer why would I want to pay with my phone number? I know if I use my Amex card I get points.. what do I get here?

2. Home Depot value. What are the metrics around the pilot and what is success? I can’t imagine how this will drive sales or margin. eBay does not market, and if they did will consumers see the price for item on eBay? eBay is a competitor to most physical retailers.. a hyper efficient marketplace. eBay has few tools to market and influence a customer during the buying process.. I’m sure PayPal has develop some very cool instore tools.. but hey Home Depot could do that themselves.

3. Consumer protections. The reason I use a credit card at Home Depot are my Reg Z consumer protections. What happens if I have a dispute? Or want to return merchandise?

4. No need for PayPal. This is actually my number one reason.. Home Depot will eventually wake up and realize that they can keep the phone number based checkout.. but use it to ask the customer if they would like to pay with the same payment instrument they used last time. There is no need for PayPal anywhere in this process. This is what happens for me at my local grocery store today (Food Lion).

Make no mistake, I do like the idea of customers giving their phone number at the POS… but it is the retailers that should use this data to make an informed decision on payment instrument choice AND loyalty incentive (example Target’s decoupled debit 5% back, or Payfone/Verizon with VZ incentives).

As a side note, Patrick’s comments on my Galaxy Nexus blog led me to update my disclosure, and restate the obvious: my views are biased (no secret to my Obopay and Square friends). Today’s blog is consistent with what I have been telling eBay’s institutional investors.. there is plenty of runway for PayPal globally.. but physical POS is a distraction and they don’t have the physical retail team to tackle it. There are no payment problems at the POS.. per yesterday’s blog, the REAL opportunity is in rewiring commerce in ways which enable manufactures, consumers and retailers to interact. eBay’s virtual marketplace is a negative to most physical retailers.. as is Amazon’s. Retailers are looking for solutions which will increase sales and decrease transaction cost. A platform which begins with a new marketing paradigm (ex. Google) is much more likely to draw participation, particularly in a pay for performance model. If this hypothesis holds, what companies are best positioned to influence a customer before they buy?

Also see Googlization of Financial Services..

8 January 2012

I’m recovering from a nice Holiday.. successfully marrying of my only daughter.. keeping a smile on my wife’s face (most important) as well on those of my children. I never thought all of that family time could make me look forward to work.. Many of my bank friends seem to be making new year’s resolutions to do something different and I’m fortunate to have them share their opportunities. What are the really big opportunities?

For those that read my blog.. I’ve been very locked-in to the concept of value proposition, and the challenges of creating a new “network” for exchange of value… with my often repeated “every successful network begins with exchange of value between at least 2 parties”. In addition to sharing ideas on new opportunities with former colleagues, I’m also about to take a trip to the Far East to meet with institutional investors. In Asia, I’m preparing for discussions which will be focused on: What are the REALLY BIG opportunities out there? Where are the sustainable bets? Where are the risks? My bias in this new year is Commerce.. and the influence that mobile will have in reshaping it.

My Investment Hypothesis:

Unlocking the “commerce” capabilities of mobile will reshape the $2 Trillion advertising market and $14 Trillion retail landscape, as new customer shopping experiences are created which leverage consumer data. 2012 will be a key year where retailers, mobile operators, handset ecosystems, banks and consumers make choices which will affect outcomes in future years.

In the US alone, we spend over $750M in marketing. Any guess how much of that is “targeted” to a specific consumer? Less than 10%.. !!

It’s not that top advertisers don’t WANT to target, but that they have no Platform to do so in the Physical World. In the virtual eCommerce world, there are many facilities for engaging influencing, incenting and paying (for performance). Data is shared from the first click… to the point of purchase across many intermediaries. In the physical world, life is much different. For those interested in this space, let me strongly recommend reading the Booz Shopper Marketing paper (just fantastic).

$14T of retail represents over 22% of the $61T global GDP.. How often do we get to talk about rewiring 25% of the global economy? This is why I’m so high on Google right now. Google currently gets only $14B of the US $750B in marketing spend, and is making strong inroads to the physical POS. (please see my legal disclosure above).

As I’ve stated before, Retailers are frequently assumed to be a bunch of back water idiots.. as a former banker I admit my mistakes… this simplified view of retail could not be further from the truth.. Retailers are on the cutting edge of competition. Competition drives data based decisions, customer centricity, daily focus on margins (as they are razor thin) and a toughness matched only in professional sports.

Retailers had to be tough and innovative… after all how do you sell a commodity on more than just price? This week’s WSJ story on Best Buy perfectly illustrates the challenges ahead for many retailers.

“I will buy it in your store…use it while I order another one for 75% less on Amazon and then return the new in the box one at your store,”

The mobile handset is uniquely capable of serving as a bridge between the virtual and physical world.. giving individual consumers access to unlimited information while they shop, not JUST price transparency, but information on quality, fashion, community reviews, availability, AND the opportunity for merchants and manufactures to reach the customer in the buying process BEFORE AND DURING their shopping experience.

What companies have the platform today? Amazon, Apple, Google, eBay, Visa.. all have elements, but the value propositions of each are widely disparate. If Commerce is to be remade, there must be a new value proposition to manufacturer, retailer and consumer. Notice I left out banks.. The problem with virtually every platform on the list below is that they have started life as bank friendly.. which destroys their merchant value proposition. Groups like ISIS are focusing on payments.. and not on a larger mobile value proposition (focusing on advertising for example, also see ISIS: ecosystem or desert).

How will commerce (and retail) be remade? I have no idea… but this will be the year which we see platforms start to gain momentum. You can guess what I’m telling my bank friends…..

8 Dec 2011

I’ve been reading some off beat stuff lately. One book “Weak Links: Stabilizers of Complex Systems from Proteins to Social Networks” was very thought provoking. As Mark Stefik (PARC Fellow) said ‘Something magical happens when you bring together a group of people from different disciplines with a common purpose.’ The combination of people, experience and approaches often leads to unexpected consequences.

As an engineer I like to solve problems.. I usually learn more from mistakes than I do from successes… but it is the learning that is fun. As an investor and entrepreneur I don’t like making mistakes… my preference in the start up environment is to have the learning cycle counted in minutes and days (vs customers and capital). I was speaking with a US Central Banker last month and the concept of “openness” was discussed. A hypothesis was laid out by the Fed “Mobile payments are not taking off because of a lack of common standards”. The Fed team is very good, the best way to encourage a good dialog is to lay out something radical; as for this hypothesis I disagreed completely. As stated in my numerous blogs: history has clearly showed that closed systems must form before open ones. I also told the Fed that the problem in US mobile payment IS NOT lack of standards but lack of a value proposition to consumers and retailers. In other words existing payment instruments solve all of my problems.. mobile payment simply does not add additional value (in isolation) compared with existing products (See Mobile Advertising Battle). In order to stimulate a change in behavior (merchant and consumer) there must be a strong value proposition. Two years ago I discussed the implications for broad payment standards in SEPA: Chicken or the Egg and in March of this year I outlined how SEPA has depressed payment innovation in the EU.

Given all of the chaos in NFC at the moment, I woke up this morning asking myself what is the “right amount” of openness and standards? How do successful networks form and mature? What are successful “open” networks? What is the first “open” standard you think of ? TCP/IP? Linux? Java? RosettaNet? EDI? Open Network? Internet? GSM? US Interstate system? SEPA? The Weak Links book opened my eyes to many new concepts, one was on how affinity influences network creation, and another on how few open networks exist in Nature. Networks form around a function and open networks are not necessarily the most efficient.

Scale-free distribution (completely open networks) is not always the optimal solution to the requirement of cost efficiency. .. in small world networks, building and maintaining links between network elements requires energy…. [in a world with limited resources] a transition will occur toward a star network [pg 75] where one of a very few mega hubs will dominate the whole system. The star network resembles dictatorships in social networks.

The network forms around a function and other entities are attracted to this network (affinity) because of the function of both the central orchestrator and the other participants. Of course we all know this as the definition of Network Effects. Obviously every network must deliver value to at least 2 participants. Networks resist change because of this value exchange within the current network structure, in proportion to their size and activity. Within the EU, SEPA undertook a rewrite of network rules and hoped that existing networks would go away or that a new (stronger) SEPA network would form around its core focus areas (SCT, SDD, SCF, ..). It was a “hope” because the ECB has no enforcement arm. In other words there was a political challenge associated with ECB’s (and EPC specifically) ability to force an EU level change on domestically regulated banking industry.. given that SEPA rules destroyed much value in existing bank networks, the political task was no small effort. We have seen similar attempts (and results) when governments attempt to institute major change in networks (Internet NetNeutrality v. Priority Routing, US Debit Card Interchange, …)

Mobile Payments Standard?

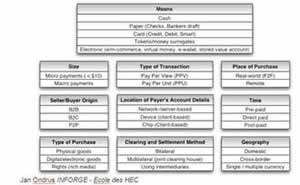

If we take a look at today’s payment networks what are the biggest problems to be solved? I have a perspective, but its certainly biased. How about payment routing and speed? These seem to be common merchant and consumer concerns. Keeping with an internet analogy, can you imagine if there were no DNS servers to route IP traffic? Every router would have to keep the directory for the entire internet not only of the final destination, but also the most effective route to forward traffic. What if the internet were not indexed? No ability to find information (thanks Google for fixing this). In the payments environment, the central assets of Visa and MA is 1) A Directory and 2) the rule that EVERY participant must route traffic through them (with a new PIN debit exception in US).

Outside of card transaction’s banks maintain their own directory for routing retail and commercial payments; this is called “least cost routing”. A key bank service I ![]() would propose (note: I’m not the originator of this idea) is a universal directory service mapping e-mail, phone and account numbers. In Australia, the banks have this today run by my friends at Cardlink and completed under project Mambo. In the US, The Clearing House (TCH) has had the UPick service completed for a number of years.. without much interest.

would propose (note: I’m not the originator of this idea) is a universal directory service mapping e-mail, phone and account numbers. In Australia, the banks have this today run by my friends at Cardlink and completed under project Mambo. In the US, The Clearing House (TCH) has had the UPick service completed for a number of years.. without much interest.

My thought here, is that rather than facilitate a EU mistake in mandating a change in all rules.. decrease the switching costs between networks so that market forces can take hold. I’m not proposing to take the directory public.. but at least give regulated entities equal access. In Australia the driver was to decrease bank switching costs, also note that Australia has no Signature debit.. just as in Canada. A common directory could also follow rule that non-regulated institutions could not hold account data (or card number).. Just as I don’t have to know my Bank’s IP address.. I could use another identifier (email, mobile, …) for online transactions. The danger for banks is that this would certainly open up the world of least cost routing to non-banks. Payments would become “dumb pipes”.. which is perhaps what it should be.

Mobile payments is certainly not critical government infrastructure. So what is Government’s proper role? Consumer data protection, transparency, regulatory requirements, equal participation/access.. ? I don’t know the answer. I like the idea of the Government creating a model service for R&D purposes.. perhaps based on Fedwire and letting non-banks have access to it… I also like the idea of a common directory.

ISIS

For 2.5 years I’ve been writing about ISIS.. I’ve always have been a huge advocate.. until lately. What has changed? My position, and that of retailers, is that today’s payment networks are heavily tilted in favor of the banks. The opportunity I originally saw for ISIS was constructing a new merchant friendly network that was an “extension” of the current mobile network which the carriers run (The original business case for ISIS is outlined in ISIS: Moving Payments from Rail to Air).

Keeping with my theme of openness and standards how is ISIS creating a platform for other to invest in? What value is an ISIS mobile payment to a retailer? Yesterday’s blog talked about the complex supply chain necessary to deliver on NFC. Don’t get me wrong, there is nothing wrong about NFC technology.. it is a very well defined specification. But it is complex.. if it was a NEW WAY of doing payments (or better yet commerce) perhaps it should have started a little less ambitiously. The team seems as if it prudently sought to reduce risk, but it also gave up on a central element to its value proposition. My analogy for today is that ISIS project is like Vanderbilt’s skipping steam and going straight for high speed mag lev in 1880…. While the entire country was growing at a 10x pace and he had no right of way..

Big projects are tough in normal times.. but mobile is changing at an unbelievably fast pace. Small focused projects are certainly lower risk when innovating at the cutting edge. Everything is changing.. how could anyone architect an open system in such a fast changing environment? It would seem that technical standards like TCP/IP or GSM were successful because of their ubiquity and distributed control. They could be used by all to create different networks with different value propositions.. which incented millions of companies and consumers to invest. I just don’t see how MNOs can create a business platform based on NFC. Their best shot may be to work with someone like Sequent Software to create an architecture for 1000s of applications to access secure element data.. instead of the one single CSAM wallet coming out in Pilot Dec 2012.

Your thoughts are appreciated

Previous Blogs (Nokia NFC Ecosystem, ISIS Ecosystem or Desert, Banks will win in Payments.. but WHICH ones?)

Notifications