This is brief.. just something top of mind. This is an extension of my previous blog this month on Remaking of Commerce and Retail. I wrote today on linked in

POS and Payment Terminal mfgs have 30+ groups trying to add coupon and payment functionality. Their message.. FIRST get a retailer that wants it. Verifone’s Verix architecture provides retailers with capability to run 100s of POS apps… but retailers are skeptical.. will “apps” drive revenue? will it confuse customers? What will drive loyalty to MY BRAND vs. some start up? who is going to manage the mess when something doesn’t work?

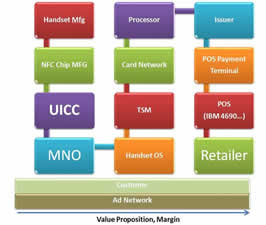

All of the Card Linked Offer companies (see my blog), PayPal, ISIS, Google, Groupon, Living Social, Fishbowl, Inxent …are trying to integrate into the physical POS. There are 2 primary options to integrate marketing into the checkout process: the Electronic Cash Register and the Payment Terminal.

I speak quite a bit with Verifone’s investors about their POS vision.. Will NFC drive reterminalization? Will payment terminals morph into a rich customer interaction environment? Big retailers like Safeway and WalMart have teams of 500-2000 developers around their core IBM 4690 ECR (ACE, GSA, SurePOS,…) and heavily customize it. Take a guess how many people retailers have in managing their payment terminal? The answer is usually zero.. The reason the payment terminal (where you swipe your card) came into being was that retailers did not want to deal with PCI compliance, so their processors (like FirstData) came in with the terminals. The Cards get encrypted at the swipe and no one but the processor has the key to unlock the numbers. The ECR sends total amount and the payment terminal tells them it is paid with an auth number. I thus find Verifone’s Verix architecture somewhat amusing… I certainly see how retailers would benefit by taking electronic coupons from this terminal (and sending to ECR), but the terminal does not give receipts and certainly doesn’t allow for matching of UPC information. Even if it did… the retailers don’t want to create a new IT team to manage this mess on a piece of hardware they don’t own.

Will Verifone sell new terminals because of NFC? YES. Perhaps even as much as a 20% reterminalization (over baseline) in next year… BUT my bet is that the POS manufactures will win the battle long term both due to retailer IT competency and the tremendous capability for POS manufactures to deliver complex business solutions (IBM is 80% of top 20 global retailers).. Things like coupons are not some abstraction… they relate to pricing and loyalty and must be integrated into a retailers price promotion strategy. Currently we are in experimentation mode… with leaders like Google, Catalina and Coupons.com.

What are the puzzle pieces that will make “rewiring commerce” work? Small companies are very challenged in delivering value within networked business. They certainly do not have the heft to create their own, so they must choose sides. Within the card linked offers space, they align to the big card networks. This alignment has implications for attracting retailers and the targeting which can be done from bank data (store preference) vs the targeting which retailers can deliver (brand and price).

In general, the Marketing and Shopping phase of a NEW commerce process requires the following

1) know the customer,

2) deliver an incentive that is relevant and prompts action,

3) in a way that is integrated to the retailers brand and price promotion strategy,

4) with a great redemption experience

5) and prove to the advertiser that the campaign was effective

The Business platform necessary to deliver on this?

1) Campaign Management

2) Customer Data

3) Advertising distribution (virtual, physical, … how do you get eye balls)

4) POS Redemption/Retailer Integration

5) Massive Customer value to change behavior (relevancy, value, usability, convenience, entertainment, social, …)

6) Global sales force that can sell to retailers

Notice that Payment is not listed.. Payment is not a problem in physical commerce. Now that Durbin allows for STEERING.. you can imagine what Retailers want to incent…

economy in 2 billion U.S. household loyalty program memberships. Edgar Dunn provide a great graphical view on the purpose of loyalty programs

economy in 2 billion U.S. household loyalty program memberships. Edgar Dunn provide a great graphical view on the purpose of loyalty programs