Short blog

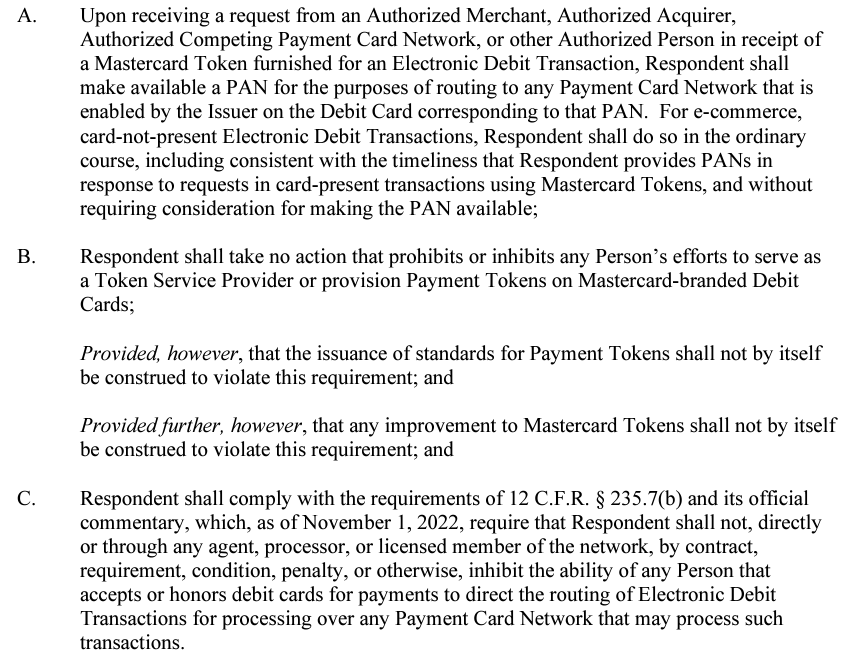

Today the FTC issued an order to Mastercard to Detokenize eCom transactions (detailed order here)

Short blog

Today the FTC issued an order to Mastercard to Detokenize eCom transactions (detailed order here)

Short arcane post. Dual routing of debit in ecom is much more complex than I thought. A puzzle and my head is spinning. Hang with me here as I don’t want to write a novel. This only applies to debit in the US.

The key take away? Competing PIN networks have new headwinds in tokenized PANs. Tokenization with a liability shift will protect Visa debit.

Continue readingThe Bull Case for V/MA (24 pages).

© Starpoint LLP, 2022. No part of this site, blog.starpointllp.com, may be reproduced in whole or in part in any manner without the permission of the copyright owner.

Part 1 – US Payments Environment covered the complexity of the US payment environment and the challenges faced by top banks in modernizing their systems (where all systems live forever). There are many types of payments: bill payments, A2A, P2P, wires.. Today the focus is on how banks intermediate commerce. Banks MUST have networks as every bank can’t connect to every consumer/merchant. Effective Bank networks (aka rails) are NOT a commodity service, but one that allows the banks to leverage their unique ability to assume risk.

© Starpoint LLP, 2022. No part of this site, blog.starpointllp.com, may be reproduced in whole or in part in any manner without the permission of the copyright owner.

Continuation of last week’s blog on “binding” and minting of tokens.

I’m currently immersed in DeFi, DAOs, Blockchain, …etc. Selected readings are at the end of this blog. Keeping Current in DeFi/DLT is almost impossible. I certainly invite comments and corrections to anything I’ve written below. While I have teams building services in this area, my perspective is biased. My purpose in writing is to stimulate discussion so don’t be shy in the comments, I welcome disagreement and discussion.

Topic today: What impacts will the $50B invested in FinTech/DLT/Crypto have on existing financial services in next 5-10 yrs? What is the summary CEO/Investor View?

© Starpoint LLP, 2022. No part of this site, blog.starpointllp.com, may be reproduced in whole or in part in any manner without the permission of the copyright owner.

September 7

This blog is dated so I removed most of the content. Key Updates – 21 Jan 2023

Part 1 – Current US Routing Rules

© Starpoint LLP, 2022. No part of this site, blog.starpointllp.com, may be reproduced in whole or in part in any manner without the permission of the copyright owner.

UPDATE – Nov 29 2022 – Note that I have conflated the relationship between SRC and 3DS 2.0. 3DS 2.0 is the authentication protocol used by SRC. 3DS 2.0 has been widely adopted as a mandatory replacement to 3DS 1.0. Part of the driver for adoption was the EU SCA mandate. SRC has NOT been widely adopted as it is a fairly broken consumer experience at the moment.

Short blog today on an example BNPL opportunity and the differences between a consumer BNPL solution like Apple Pay Later and Merchant integrated solutions from providers such as Affirm (or SQ/Afterpay see Three Flavors of BNPL). Today Air Travel and Vacation packages are the focus.

Please purchase a subscription if you would like access. Exception for friends I’m connected with on LinkedIn, please send me an email and I will mail you credentials. If you are having difficulties accessing content please clear cache and log in again.

Continue readingShort blog today as opposed to the 9 page monster in identity and attribution Friday. Today I’m providing my thoughts on what a consumer data bureau would look like. Summary: Banks have a unique opportunity to create a consumer data bureau and be the key “switch” for regulated and permissioned data. Will they seize it?

Per blog yesterday, everyone has a partial view of you based upon their observations and what you trust them to hold (see Payments and Observer Effect). The more often you interact with a single entity, the more they learn about you. Today Google and Amazon know you much better than your bank. Any unique insights that a bank may have is limited by their ability to take part in that transaction. Thus entities, with the ability to initiate transactions, have the most control (summary of Identity will Define Future of Trust Blog).