Short blog

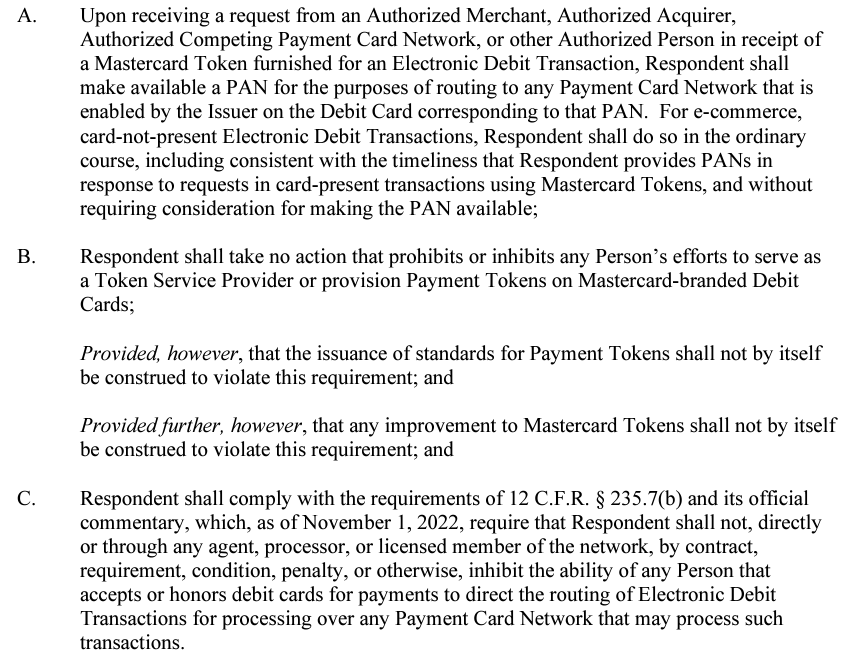

Today the FTC issued an order to Mastercard to Detokenize eCom transactions (detailed order here)

Short blog

Today the FTC issued an order to Mastercard to Detokenize eCom transactions (detailed order here)

Short Blog – Chrome AutoFill

I missed a key development 6 months ago: Google’s Chrome autofill began using network tokens in May 2022 (see article) after the Google Wallet relauch which was announced as part of Google I/O. Google now allows issuers to provision cards to the mobile device and to the browser desperately (see Web Push Provisioning) using network tokenization services (VTS/MDES). I discussed this in detail in my 2016 post Browser Tokens.

A Correction to previous blogs. Google’s Chrome autofil has network tokens, but (within the US) does not obtain a liability shift. For Google autofill to get a liability shift (within network rules), they would need to enable the 3DS 2.2 authentication features. Exceptions to 3DS 2.2 are where Issuer has provisioned card with Cryptogram (ie ApplePay card provisioned into wallet by bank). See Mastercard API doc for detail.

Continue readingShort arcane post. Dual routing of debit in ecom is much more complex than I thought. A puzzle and my head is spinning. Hang with me here as I don’t want to write a novel. This only applies to debit in the US.

The key take away? Competing PIN networks have new headwinds in tokenized PANs. Tokenization with a liability shift will protect Visa debit.

Continue readingHappy After Thanksgiving! Hope everyone was able to enjoy a wonderful time with family and friends. Today is the 3rd installment of the series, a long blog.

The next big network wave is here. Call it web 2.5 or 3.0, but the integration of payments into “everything” is a major event. Payments are the “trust layer” that TRANSFORM anonymous nodes providing uncertain service into known, defined and guaranteed service providers. Effective communities require value exchange and “trust”. The payment trust function enables networks to evolve from “cost free” discovery and information sharing, into transactional resource/service exchange: from read-write to read-write-execute. Sure we could call the wave “trust” but the only ubiquitous “trust network” is payments so I prefer to keep payment wave as the naming convention.

Per my June blog BNPL – Travel Example, I laid out how Airlines were a logical focus for BNPL. It seems that Issuers are either reading my blog, or coming to the same conclusions as SRC is likely to launch first with Airlines.

Continue readingShort Blog

I’ve had quite a few inbound calls on Durbin and Debit in eCom so I thought it was time for a short blog. Note this is my 90% confidence view talking to 3 of the top retailers and 2 of the top processors.

Trust in a transaction. In another one of my favorite books (Design Rules: modularity) there exists the concept of trust between physical components of an integrated system. This book stands in contrast to Nobel Economists’ work in defining the “Firm” and organizational boundaries in Transaction Cost Economics (TCE). But the technical theory of modularity is amazingly consistent with the concepts of “boundaries” in TCE. In modularity, there are 4 core rules for separating technical components:

Continue readingFree Article

Continue readingThe Bull Case for V/MA (24 pages).

© Starpoint LLP, 2022. No part of this site, blog.starpointllp.com, may be reproduced in whole or in part in any manner without the permission of the copyright owner.

Part 1 – US Payments Environment covered the complexity of the US payment environment and the challenges faced by top banks in modernizing their systems (where all systems live forever). There are many types of payments: bill payments, A2A, P2P, wires.. Today the focus is on how banks intermediate commerce. Banks MUST have networks as every bank can’t connect to every consumer/merchant. Effective Bank networks (aka rails) are NOT a commodity service, but one that allows the banks to leverage their unique ability to assume risk.

UPDATE – Nov 29 2022 – Note that I have conflated the relationship between SRC and 3DS 2.0. 3DS 2.0 is the authentication protocol used by SRC. 3DS 2.0 has been widely adopted as a mandatory replacement to 3DS 1.0. Part of the driver for adoption was the EU SCA mandate. SRC has NOT been widely adopted as it is a fairly broken consumer experience at the moment.

I’m at M2020 today and it has been a “back to normal” fantastic event. Let me put my “merchant hat” on for a story from their perspective.