© Starpoint LLP, 2026. No part of this site, blog.starpointllp.com, may be reproduced or retransmitted, in whole or in part, in any manner without the permission of the copyright owner. Also, see our Legal/Disclaimer (this is a highly opinionated and partially informed blog). Enterprise readers, please consider an Enterprise Subscription (not required for Starpoint Clients).

Executive Summary

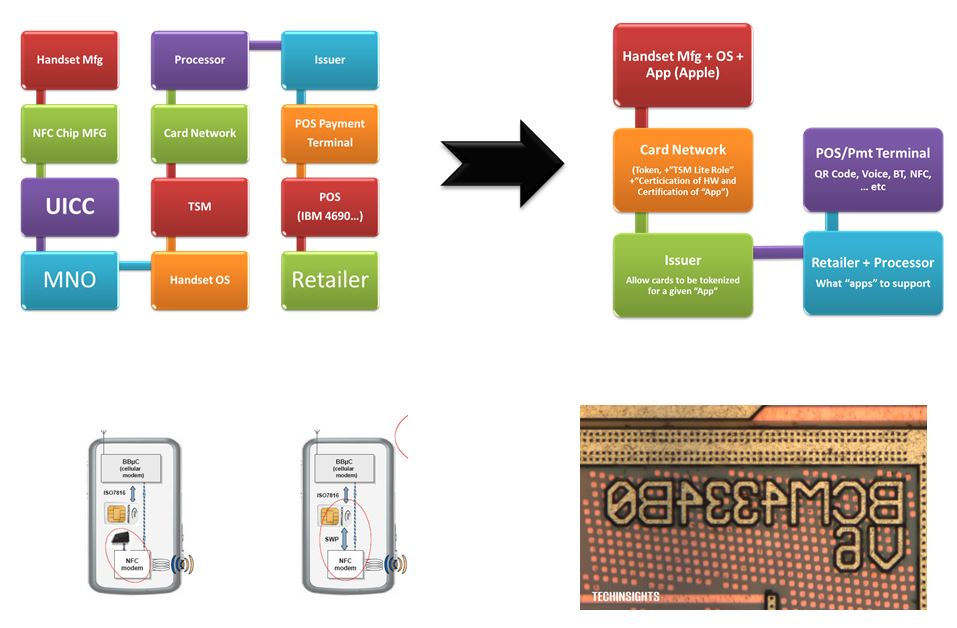

I’m fortunate to chat with a diversity of large payment network stakeholders. As most of you know, I view the challenge in payments more from a political/incentive viewpoint than a technical one. The alphabet soup of new standards is hard to keep up with, but be assured that each one has a proponent (who benefits) and a group of resistors. Innovation in a network is hard, as existing stakeholders have built assets and competitive positions based upon how things work today. Today’s blog covers DPCs. DPCs may not be the biggest threat, but they are the newest. I’m not going to attempt a deep tech dive into DPCs; my effort is focused more on the challenges faced by any new payment innovation to gain traction and scale. Network effects are hard to beat!

Why read this blog? My readers know I view identity and authentication as part of the core “bundle” of payments, and Visa/MA are the de facto identity infrastructure of the internet because they unlock the power of banks (ie KYC) within a commercial framework with active governance. Today we are breaking down the latest “threat”: Digital Payment Credentials (DPCs) within Agentic(ie Gemini, GPay). The quick summary is that DPCs are an amazing technical innovation without a commercial framework or active governance, and thus will be challenged to operate separately from established networks (just like Stablecoins). This 23 page monster blog is a breakdown of the politics and the tech.