Big news from PayPal’s earnings yesterday was Amazon taking Venmo. I wanted to summarize the 15 tweets on the topic and provide a little more background into the dynamics.

Amazon is an amazing company from a people perspective, perhaps the best TEAM I’ve had as a customer. They always proceed within a plan and purpose. So why Venmo? As I related 2 weeks ago, Amazon is working to reduce the costs of payments. They have managed fraud down to 3bps.. So why can’t their processing costs look a lot more like Walmart? They have been successful in achieving this in EU (Sepa DD) and India (see blog), but the US remains (by far) the highest cost geography.

You need to be logged in to view the rest of the content. Please Log In. Not a Member? Join Us

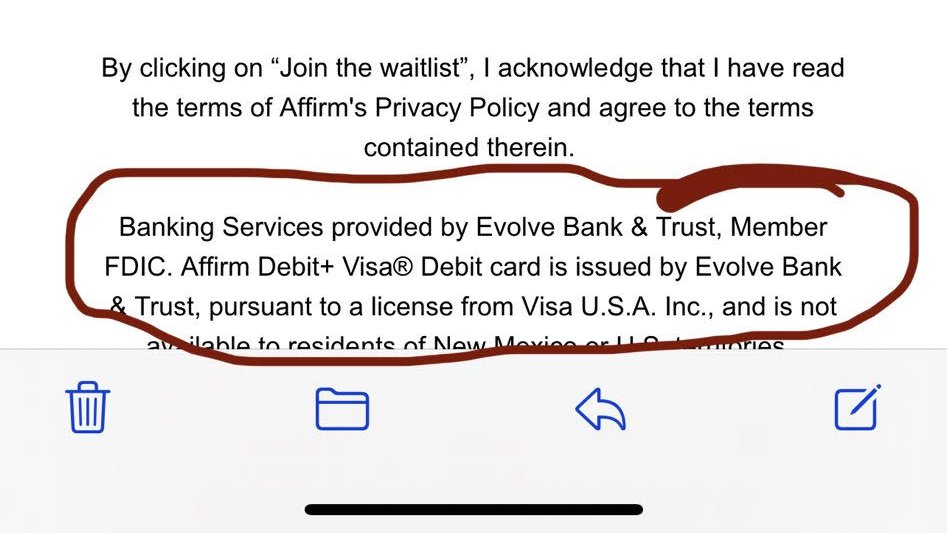

Update 8 November – Original post is below the image.. I had doubted Visa’s support here. But clearly this is a real product.

Affirm Debit+ is a decoupled debit on the Visa network with Evolve Bank as ODFI/Issuer. I doubt if Visa fully vetted this product.. it MUST have “slipped through”. For more info see Affirm’s investor day presentation.

Per my blog last week, my hypothesis is that the new Affirm Debit+ will be revolutionary.. which is why it is currently causing a massive firestorm amongst Banks. Today I want to drill into what I believe the value proposition will be (my hypothesis) and why Visa had to support this.

Today Affirm is “limited” in growth to the merchants it can directly integrate to. How can they solve this problem? Create a consumer “pay anyone” product that lets the consumer pick and choose what items they want to finance after they purchase them. Connect any of your bank accounts or all of them.. Finance anything you buy on improved terms. Affirm will also work with Stripe and others to create an improved checkout process, which will improve both conversion AND consumers ability to purchase (ie underwriting). The first mover advantage will be tremendous and step on much of the Neo Banks (already slim value prop).

You need to be logged in to view the rest of the content. Please Log In. Not a Member? Join Us

At Money2020 this week and I have to say I’m having a blast. Seeing friends face to face and getting back to “normal” was well worth taking my first plane flight in 20 months.

Visa Announces earnings today at 5pm, the big question institutional investors are asking me is about the Amazon – Visa discussions. It is a big game of chicken right now, with earnings ramifications. To understand whats going on here, let me attempt to give some abbreviated history.

You need to be logged in to view the rest of the content. Please Log In. Not a Member? Join Us

Get into the START of a consumer shopping experience

Enable a new mobile first shopping experience – focused on small merchants – from beginning to end (like Alipay)

Pinterest

“Inspiration to Action” – They are missing the action beyond a ad click.

Stalled user growth

50%+ Revenue growth with consistent operating loss.

454M Users with ARPU of $5.08/User vs PayPal’s $21/User

Ad Growth to Action. Advertising business with solid advertising relationships with CPGs and large retailers. However you don’t click to buy from a CPG.

Needs platform to complete consumer journey.

You need to be logged in to view the rest of the content. Please Log In. Not a Member? Join Us

Thought I would give more detail on whats going on with V/MA, Issuers and Apple (from WSJ article yesterday Apple Pay Fees Vex Issuers). Perhaps I’ll collect a fee from the WSJ.. odd that I mention Apple Pay fees on Monday to have it come up in the WSJ on Tuesday. Oh well..

You need to be logged in to view the rest of the content. Please Log In. Not a Member? Join Us

Most of you techie’s out there had a physics class at some point and can recall the Observer Effect in Quantum Physics: the act of observation can change the measured results. Observation in payments has become the second largest driver of margin and has enabled many new specialists…. so I thought I’d outline some broad thoughts and tell a few stories.

Why is observation important? Payment behavior is truth marked data of what a consumer actually did (offline). While I may search for Ferrari’s, or visit dealership (mobile location) what I actually bought is much more important in predicting behavior and evaluating risk. Purchase data is the most valuable data for that reason (and issuing banks had a lock on it.. Until about 5 yrs ago). The lock has been broken and payment data has become the “missing link” to unite heterogeneous data sets.

You need to be logged in to view the rest of the content. Please Log In. Not a Member? Join Us

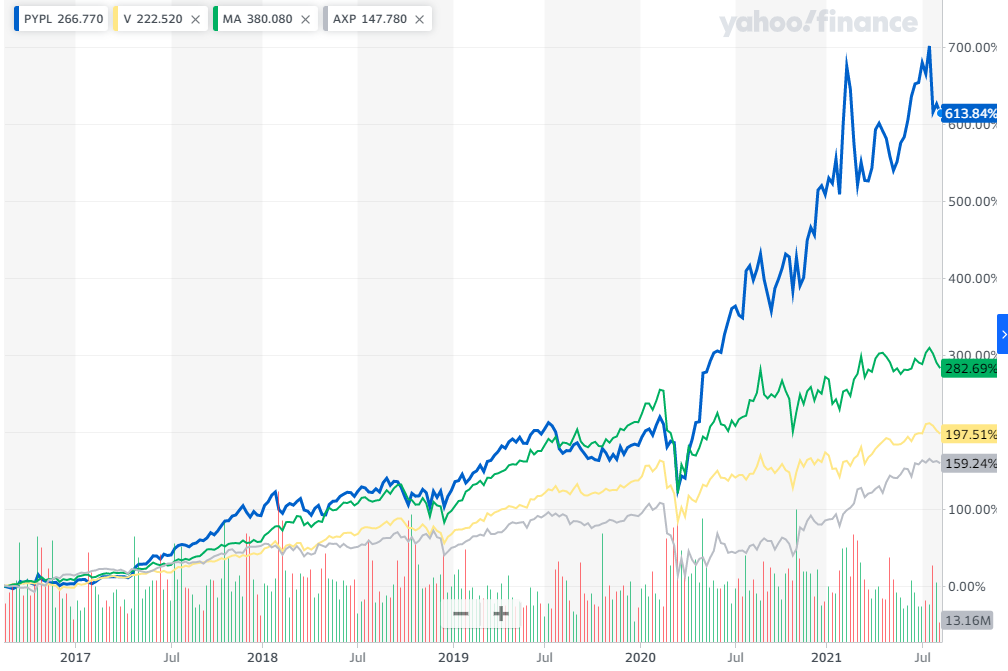

PayPal has been my #1 holding for last 5 yrs, and it has been on a fantastic ride… especially so over the last 18 months! (see MVP – Continued Domination for more).

Paypal announced 2Q21 earnings 2 weeks ago (7.28). TPV growth was 40% with eBay, 48% without out, while sales grew at a 32% clip without eBay versus 19% with. Earnings? Not so much as margin erosion has hit the business. One core driver of margin has investors particularly concerned: “Take rate” (net merchant revenue less cost to clear payments) fell from 2.21% in the fourth quarter of 2020 to 2.11% in the first quarter and 2.01% in the second quarter.

You need to be logged in to view the rest of the content. Please Log In. Not a Member? Join Us