Short Blog

Continue readingAgentic Commerce – Hype and Reality

Reply

Short Blog

Continue readingUS Payment Infrastructure is in the midst of completing a major renovation.

Let me preempt the #1 question most of you are about to ask “are card volumes at risk”? Nope, why on earth would banks want to walk away from the most profitable retail banking product in the history of man (see Future of Retail Banking)!?

© Starpoint LLP, 2025. No part of this site, blog.starpointllp.com, may be reproduced or retransmitted, in whole or in part, in any manner without the permission of the copyright owner. Also, see our Legal/Disclaimer (this is a highly opinionated and partially informed blog).

My estimates for how US eCom market share will shift in next 3 yrs are at the end of this blog.

eCommerce is not a single monolithic market. There are many “segments” to optimize that vary by geography, retailer type, consumer device, customer type (guest vs loyal), transaction type (recurring vs new), ad type, payment type,…etc. A great source of this information is Monetate (highly recommend). For example, let’s look at conversion rates by industry, device and region.

Continue readingLet’s talk about tokens. When discussing tokens and payments, it’s important to clarify which category of tokens you’re talking about. Today, I’m not discussing NFTs; instead, I’m discussing card network tokens. It’s hard to believe I’ve been writing on this subject for almost 15 years. For a historical refresh, here are a few of my old blogs

Continue readingAs we wrap up 2024, I thought I’d outline a few key areas I’m tracking and things to look for in 2025.

Continue readingBull Case For Visa and Mastercard

Very Long Blog. 4 Page Exec Summary. Feedback appreciated. This blog has been my “blocker” as I’ve iterated over the last 7 months. I’ve thinned this down from 31 pages (which no one would read) to 23. No I will never write something this big again.

The thoughts below are an update to my 2016 Small Wins, where I outlined how the forces that have driven scale, and shaped organizations, are atrophying (Transaction Cost Economics, asset intensity, information intensity, finance… etc). Paul Graham’s calls this change Refragmentation, I call it Transformation of Networks.

It’s as if the gravitational constant (the big G) is changing and new forces are driving the formation of new networks influenced by a rapidly evolving world of “weak links”. Information intensity has moved beyond “tweaking” 100 yr old business models to transform the design of industries, communities and people.

Whereas the 2016 blog was more about the “possibilities” enabled by tech, this blog is about the reality of how things will evolve.

© Starpoint LLP, 2024. No part of this site, blog.starpointllp.com, may be reproduced or retransmitted, in whole or in part, in any manner without the permission of the copyright owner. Also see our Legal/Disclaimer (this is a highly opinionated and partially informed blog).

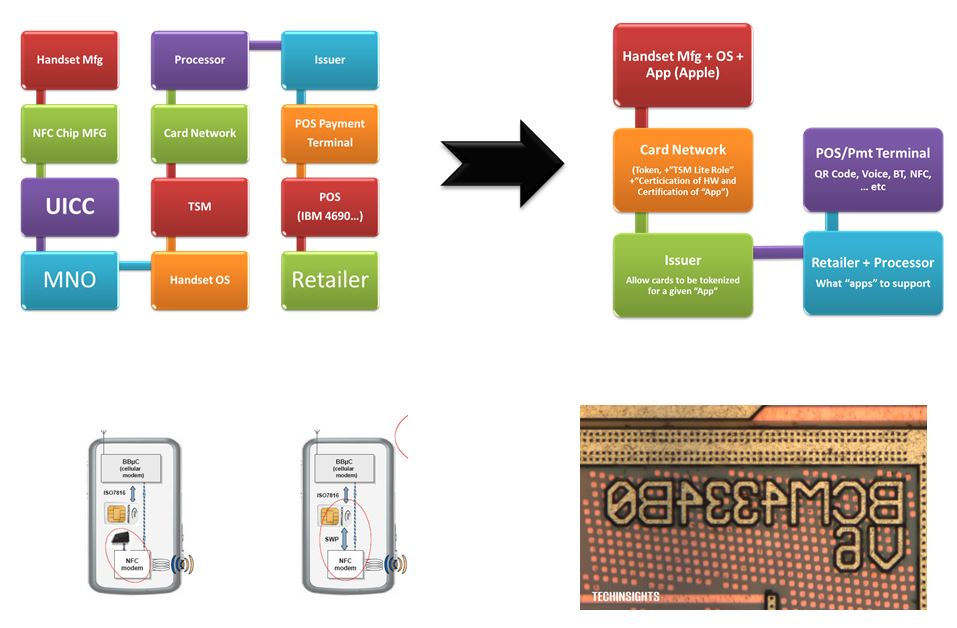

What are the core functions of a digital wallet and what will the future bring now that Apple has opened up their Secure Element (see blog)?

I’ve been writing about wallets for over 12 yrs. Let me recap some history

US Focused Blog

Last week I wrote about 3 banks live with TCH RfP, today’s blog covers

Notifications